Bank Stocks! TSLA Earnings, CVNA Craziness

Everybody, it’s Pete. Welcome to today’s episode of the Daily Ticker, joined by David trainer from New Constructs. Thank you so much, David, how you doing today? I’m doing great, Pete.

How are you doing? I’m market’s going up again nine days in a row for the dow. I mean, unless you’re trying to short this thing and you’re drowning right now, I think everything is okay right now. It’s a matter of timing.

We get a lot of people in our community right now where I want to get in. I want to get in. We get in the stocks up 14 days in a row.

And I’m like, risk reward is not on your side right now. Pick a side and pick a spot. The spot right now is off a little bit, but I think today we’re going to dedicate to earnings and some crazy numbers that we were just talking about that almost don’t make sense.

Obviously, netflix came out. The whole password sharing thing looked good last quarter. They’re actually getting hit now.

Last I looked, they were down $28. Now they’re down $32 7%. So from one quarter to the next, where the password sharing thing was awesome, next quarter it doesn’t look so awesome.

So you got to really be on top of your game. But I think the two stocks that we want to talk about today in a big way, Tesla with margins, second quarter in a row. Tesla is big numbers on the top line, but margins are shrinking.

And it’s, in my opinion, a little bit of a magicians act right now where they’re buying the CEO celebrity, maybe a little bit of the other companies using their charging stations, and maybe they’re kind of getting a little bit of a network effect off of that. Maybe it might have a little bit of an opinion on that. But look, I’ve been in business a long time.

You hear margins are going down. That’s not good. The stock has pretty much not moved at all right now.

But one of the other ones that I definitely want to get into is you called it the meme stock of de jure right now, which is Carvana, I think recently. Now it’s gone from $10 to 52 in five weeks or something along those lines. You want to start with that one? Sure.

Yeah. Carvana is one of our original zombie stocks. We put it in the danger zone, I think, when it IPOed.

Pete, a zombie stock is a business that’s losing money and doesn’t have enough cash to support that burn rate for more than 24 months. I think Carvana is down to a pretty low number. But they did what all smart meme stock companies do.

They saw their stock price go up, and they sold shares. So I don’t know if they’re going to be able to last a lot longer now because they actually got some cash in the books. But the business model is broken.

It’s never worked. As we pointed out in our first report on it, they haven’t made any money in the most densely populated, larger metropolitan markets, and now they’re moving into the lower margin markets, and the margins are already negative. So it doesn’t make any sense.

I’m just going to pop it on the screen here, Dave, just to give everybody an idea of what we’re talking about in case somebody happens to be watching this at a later time. Carvana has gone from $5 in May, which is not that long ago, to today. It’s at 59 and change right now.

Just to give everybody an idea of the size of this move right now, just to put it in context and something we actually pointed out from a trading perspective, a little bit different point of view from the investing side is you start to see the size of the candles and lack of institutional attention. All of a sudden, the candles are getting a little bit bigger, and you know something’s coming before it even happens. These months and months of accumulation.

And now you could even just see clearly the size of these, which were tinier. A lot more people are involved. Now.

The question that everybody’s going to have at this particular point, are you going to be the one who’s holding the bag after the stock now has gone? I mean, actually, I’ll just give you the percentage right now. We just said from $5, but if we’re going from mid April, it’s a 736% move. Yeah.

That’s going to track a lot of FOMO. Yeah, that’s what I’m basically getting to at this point, where there’s a difference between it’s going up versus it’s a good trade or a good investment when you’re about to hit that buy button, and I think that’s a big part of it right now. We can all throw around the word valuations, intrinsic value, whatever definition undervalued you want to put on it.

Is it a good opportunity to get long right now when the stock’s just gone up 736%? Yeah, and I think we’re about to get some rather for the market. I think it’s good news, but I think the market is going to get some unpleasant news around what the Fed’s going to be doing here in the next couple of next week or so. I think the Fed’s going to hold the line and the liquidity environment is going to remain tighter, which means it’s less likely that or that Carvana is going to be able to roll over their debt again, which they were able to do.

This new debt restructuring deal doesn’t lessen the debt, it changes it from unsecured to secured, which is not a good thing. The debt holders are going to own all the cars, and that was over a billion dollars, if not mistaken. Right.

That news came out yesterday. Yeah. And so this is not necessarily a great deal.

And it was good that they were able To Sell Stock. I mean, I feel sorry for the people that bought this stock. That’s just nuts.

But look, they got it done. Wall street made some money. We know the insiders are making a lot of money.

I just pray that not too many individual investors get caught up on this one. Yeah. So again, just to be clear for everybody here, everything we’re talking about here is for educational purposes.

It’s up to everybody to make their own decision. What we’re talking about now is if you are looking to buy the stock after a 700% move, you just have to really ask yourself before you hit that buy button, what is the next likely move? For the risk to justify this trade? That’s really what we’re talking about right now. Just thinking about what’s the likely move in the time frame that you plan to be in the trade.

That’s all we’re saying. We’re not saying do or don’t. We’re just throwing some ideas out there.

So I guess the other big bad boy that we’ve been talking about probably for a while now, and I think who’s not talking about it right now, which is Tesla. The fact that the stock has gone from 150 to 290 again in a very short period of time. At what point does the stock no longer be a smart play for either value investors or growth investors? There has to be a different story.

I posted that on Twitter yesterday. What is the story that’s going to make the stock that has now doubled in a very short period of time continue to go up? So again, we’re talking about risk reward. So if you have some stuff you might want to share on that, David, both visually and as far as the valuation on where Tesla is right now, that would be awesome.

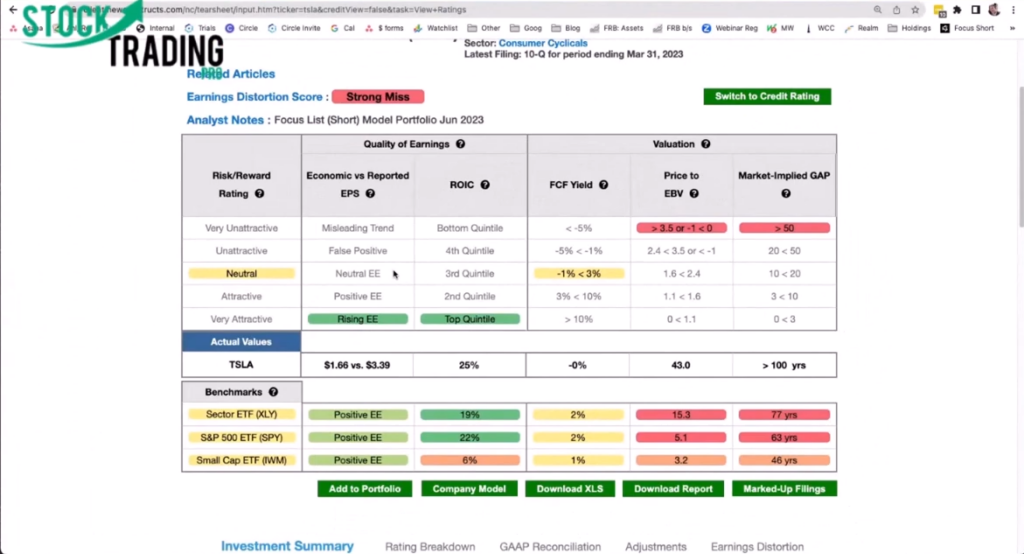

Yeah, sure. I mean, we can kind of go to the rating page here and you can see that. Look, the quality of earnings at Tesla looks good as I think a first mover should.

Right. I mean, look, they were the first to be in the market, so they should look great. The valuation is really where things get really kind of I would say absurd.

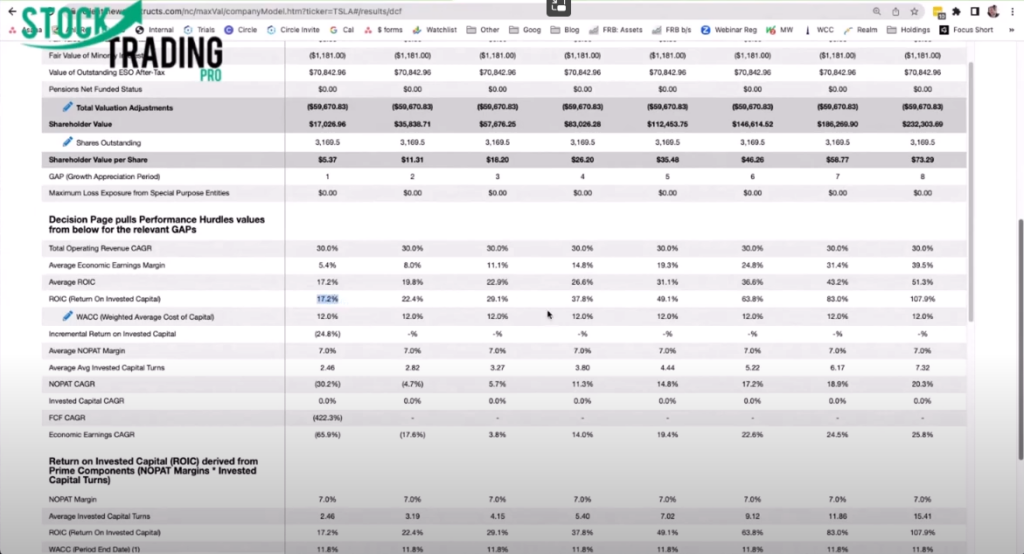

And when you build a model that plots out sort of the implied values of the business over time, I jacked the revenue growth numbers way up so we could get to this nearly $300 stock price. And what it shows is that you got to believe that the company is going to grow revenues at over 25% compounded annually for nearly 20 years. So let’s just say 25% compounded annually for 20 years.

You know how many companies in the history of the world have ever done that? I don’t know if any have. Certainly not a large cap company. Just repeat that one more time.

I want the significance of that. To really hit home, they got to grow at 25% compounded annually for 20 years. Grow revenues.

The top line. And what’s really interesting is when you start to kind of then figure out, well, what does that mean in terms of vehicle sales? Even if we assume that only 60% of those revenues are for auto vehicles or for vehicles, right. That means they’d have to sell almost 25 million cars at an ASP of around 45 grand.

- 45 grand. And by the way, the total market and by the way, Toyota has only sold around ten or 11 million cars in 2022.

In 2023. And that level of sales is like 40% of the entire expected electric vehicle market, based on the International Energy Associate Agency’s estimates. Right.

So, I mean, it’s pretty nuts. The average new car price in the US is $48,000. $49,000.

If they sell at that average price. And by the way, their car is a little more expensive, they sell 21 million vehicles. That’s 40% of the market.

If they sell at the average new car price for the world, which is $28,000, they got to sell 35.9 million vehicles. And that’s 68% of the market.

68%. 68%. And that’s assuming only 60% of the implied revenues are attributable to the auto sales.

The rest of the business comes from whatever you’re going to make up. Magically, Pete. Right.

Oh, it’s going to be insurance, because that’s such a high profit business. And by the way, the return on invested capital in this scenario, this 25% compounded annual revenue growth for 20 years, the return on invested capital that we’re looking at, or the implied that the company has to also achieve here’s, the return on invested capital in this model. So going up to 17.2,

which is a really heady number, but you see it’s climbing really fast. I mean, only a few companies in the S and P 500 have returns on invested capital this high. But when we go out to year 20, where we’re getting to close to $300 a share here, right in the model, we’re looking at 900 or 1000% return on capital.

Wow. To really emphasize again, Pete, like what you were saying before, 25% compounded annual revenue growth for 20 years is one thing, but to do that while also seeing your returns on capital improve is to assume you have zero competition on two levels people trying to just get into the market and people trying to comPete on margin. It’s gotten to be so absurd that for the longest time, I think the valuation of the stock has been disconnected from fundamentals.

And you’re right, it’s a musical chairs game. Who’s going to still be holding the stock when all of the hype has run out? So that’s an interesting topic. Is it the CEO, celebrity CEO that everybody’s buying into, or is it the company at this particular point? I mean, it seems to be more they’re buying the CEO than the actual numbers because those numbers are borderline mind boggling, for lack of a better way of putting it.

I don’t want to use a financial term. I just keep it psychological. Because, again, everything we do is about what’s likely to happen, and again, whether that’s likely to happen over the next week or likely to happen over the next 25 years.

That’s the ultimate reason we’re choosing to accept risk, what’s likely to happen. But I think a lot of people, unfortunately, buy based on what they want to happen, not what is likely to happen. And that likely to happen is why we choose to accept risk in the first place.

That’s right. I mean, investing is a risk reward analysis game, pure and simple, unless you’ve got a crystal ball that’s going to tell you what the future is. We’re dealing with an uncertain future, which means there’s risk.

I can’t predict the future. I don’t pretend to. And I love telling my analysts when they start in our training program, I always say, would you rather be a fortune teller or critic of a fortune teller? And they’re always like, Well, I guess I’d rather be a critic.

I’m like, that’s exactly how we roll. Mr. Market is our fortune teller.

He’s giving us a price every day. It’s up to us to determine how optimistic or pessimistic Mr. Market has been.

And we like to focus on the extremes where we just reverse engineer the expectations baked into a stock price to get a sense of whether or not the future cash flows implied by that stock price are realistic compared. To what the company’s done in the past or in a case like Tesla or even Carvana are comparable to anything that any company in the world has ever done. With Tesla, you’ve got sort of amazing just expectations for performance that is, I think, so far beyond what any company has ever done.

It’s mind boggling, but you get the idea. It’s just a much smarter, I think more deliberate, conservative, appropriate, I think also, Pete, it’s just a more humble way. I’m not going to pretend I can predict the future.

Let me focus on what I can do and what we can help investors do. And this just feels to me it’s just a better way of doing things. So let’s go to the other side.

A couple of weeks ago, we spoke about some regional banks that were about to report. So we have a couple to discuss today. Schwab is not a regional bank, but Schwab actually came out with some good news.

They got caught up in the tsunami of the regional banks, got crushed. Schwab came out, but all credit where credit is due. You spoke about Zion a couple of weeks ago.

Let me just show that on the screen real quick. And then you could take it from really, really nice, what we call in our universe accumulation, where the stock got caught up in all that fury. First part of the year, first quarter of the year and really hasn’t done much since then.

But last couple of days, finally taking out levels. And again, we like to keep support and resistance as simple as possible, where’s the significant price sellers did something and buyers were finally able to punch it through there. Earnings came out after hours and now up 6% on top of 6% in regular trading hours.

So 12% in Zion. And again, full credit to you. You spoke about that a few weeks ago.

You expected them to come out with positive perception. Let’s just say perception mr. Market does whatever the heck he wants, but the numbers were just implied based on what they normally do, that the price was just too suppressed based on what was likely.

So maybe, David, you want to do a little bit of a rundown on Zion? Yeah, I’d love to, Pete. We made it a long idea. It’s actually on our focus list.

You can see the rating here for Zions is very there’s. Everything looks good here. Great profitability.

Very different from Tesla, where you see the really high valuation, the red warning valuation stuff. But this price to economic book value is one of my favorite ratios because it’s just a great way to get a handle on stocks and their valuation. And at the current price, this is yesterday’s close, right? That price, anyway, implied that the company’s profits were going to permanently decline by 70%.

Maybe Mr. Market is being a little too pessimistic here. Right.

And that’s just a much better risk reward situation, and that’s what we’re trying to help people with. Pete, I have to tell you, too, we also made Schwab a long idea a little before Zion’s. In fact, we did not put Schwab on the focus list because I think it doesn’t look as cheap as Zion’s.

But we just saw an opportunity where the market was throwing some of the babies out with the bathwater and the bank and banking businesses. And we reiterated our call on JP. Morgan, which has been a great call.

And then we added Schwab and Zions to our long ideal list. And look, you’re dealing with businesses that are generating great cash flow trading at great valuations or super cheap valuations. Your risk reward is tremendous.

So just one other company in the financial area while we’re on this, and I know we didn’t prep for this, so I just want to be clear about that. Goldman Sachs is having a tough year. They reported they’ve shown relative other than probably the first month of the year, goldman Sachs has been relatively weak to the entire market.

I know financials haven’t exactly had a great year, but a lot of the financials and the XLF have really perked up in a big way over the last six to eight weeks. Goldman came out today, and the market not in love. I mean, yesterday, Morgan Stanley just absolutely blew it out of the water and flew to the upside.

I know on our side, a lot of our members just had a really amazing day on the Morgan Stanley earnings, and Goldman Sachs is basically a dud this year. Do you see anything wrong with their business model in general, or what would we need to see to them to finally get out of this doldrums for the year? Yeah, I think the knock on Goldman, by the way, it looks attractive. It’s not as nearly as cheap as some of these other stocks, but great economics.

And on a relative basis, though, I would tell you that the issue, the knock on Goldman is that they don’t know who they are anymore and they tried to do this thing with Marcus and get in the consumer thing and I think it really blew up in their face. The consumer division I think, was a big loss for correct, correct. That was the consumer not they don’t have the culture for that.

It’s not what they’re about. So Goldman’s got to figure out where they’re going to grow because I think the legacy securities businesses are in kind of a long term secular decline. I think that’s part of why we’re seeing a bunch of IPOs here before the summer hits.

I think bankers know that the good old days are coming to an end. Technologies like ours are making it increasingly difficult for them to pass off these really bad companies to unsuspecting retail investors. Because we’re educating people about what’s really going on.

And we’re able to read through all the footprints, the footnotes and fine print footprints. That’s a nice amalgamation. And give people the honest truth in a way they couldn’t do that before.

And I think that just means that the clock is ticking. For how long? Wall street can kind of keep up the ruse, and that just means they’re pushing more bad product out. And Goldman in general has got an existential problem like, who are they going to grow up and be? The consumer business didn’t work.

The legacy securities businesses, yeah, they’re the king of the mountain. They’re the best at that. But those are in kind of a decline, long term secular decline.

So it’s trading right now as if its profits are going to be flat to down about 10%. That might be a fair valuation. The right price at this moment go to another one in that area again without necessarily doing any research.

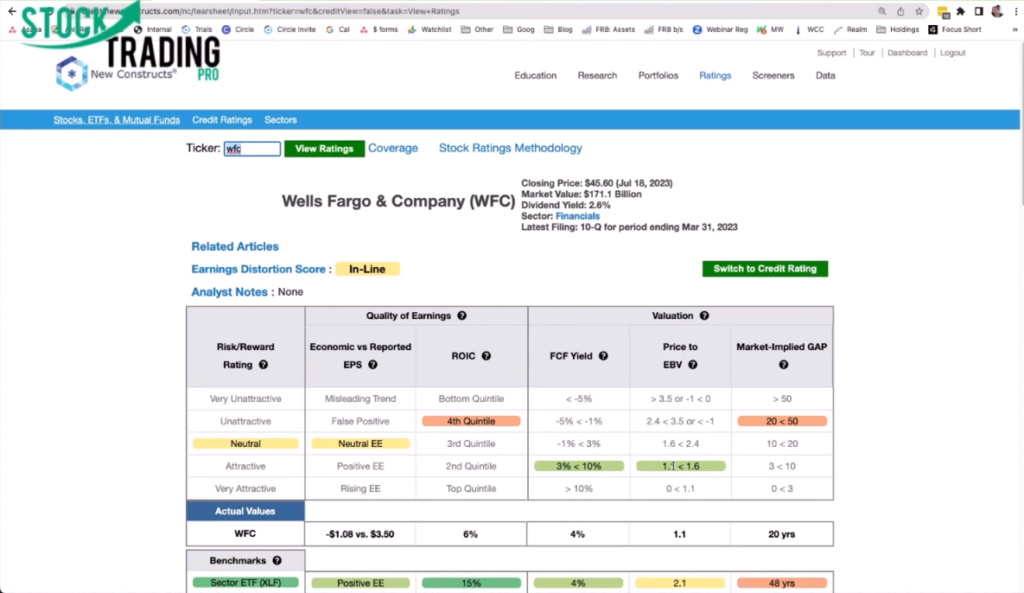

Is Wells Fargo beyond the non love from Wall Street? That was a hangover for a while. It seems like they’re getting a little bit of bullish juice here. Yeah, we can take a look at the rating on Wells Fargo.

Right? So, I mean, Pete, it’s easy for us to pull that up, right? I mean, I was just at GS a second ago. I told you the price to economic book value at 0.9. Maybe there’s not going to be a lot of growth.

Then we look at wells Fargo, and for the longest time, they were a leader in return on invested capital. We thought it was a much better business than it was. We turned out there were some issues with that Wells Fargo business, but then looking at valuation doesn’t look that cheap.

So I wouldn’t be a big bull on Wells Fargo. I think they’ve still got some compliance and cultural issues to work out. And then the profile of the business at this point doesn’t look that great.

I do think that there was a recent upgrade on Citigroup, though, because it was so cheap. Yeah, it’s trading as if profits will permanently decline by 50%. So that to me is a little bit better situation.

Now, the market implied growth appreciation period is still pretty long, so I’m guessing that there’s quite a bit of revenue decline and margin decline already baked in. Maybe this 0.5 is a little bit more reasonable.

I, for one, when we think about financials, wells Fargo doesn’t really make the list. Goldman used to make the list until the consumer thing imploded and they lost a growth story. We love Morgan as a best in breed, and then we love these Schwab and Zions and some of these other really super cheap regional banks.

So what is it about Morgan’s business model and numbers that you like so like? It’s the best in? I mean, they do so much so well. They have really high returns on invested capital. I think their compliance is among the know.

I have a lot of respect for Jamie Dimon and the way he runs the business and his background. I remember him all the way back at Bank One back in the 90s. He was a great operator, and I just think he genuinely ensures the culture does not breed the kind of cowboys and risk taking, because a lot of these operators, these traders are under the assumption, and mostly it’s valid that they can enjoy upside without taking downside risk because the government that work for SVB correct.

Yeah, I’m a big Jamie Dimon fan myself as well. I have a bunch of books on I’m going all the way back to when he and Stanford Wheel, he was his mentor. And if I’m not mistaken, it was Citigroup, right, that they were with each other.

I think so. I don’t remember who bought Bank One? Was it citigroup? Who bought Bank One? Oh, gosh. EAB.

There was a couple of banks that got absorbed back then. So I remember I was actually trading at a building in Nassau County on Long Island, and they changed it from one bank to the other for some reason. I can’t remember what it was.

But, yeah, I’m a big Jamie Dimon fan, and the Morgan stock is one of the cheapest. I mean, it’s even cheaper than so, you know, we really love how it’s cheap. It’s still a really cheap stock.

And I’ve said that I think this is better than an index fund because I think the beta is lower. And look, even if you’re in the S and P 500, you’ve got a bunch of junk and they got Tesla got a lot of risky stocks in there that I think are going to create more volatility in that index than what we’re going to see with the JPMorgan, which is good old banking. It’s a business, people need money.

That’s for, you know, I think gains accrue to the best players, the best run businesses in a big way. Over time, you’re going to acquire more talent, which is going to help you run your business better and you’re going to put your competitors at a worse position. And I think Jamie gets that and I think he understands that he’s building a real fortress.

Just I’ve been impressed for probably a lot of the same reasons as you, Pete, that running a good business and running a good business is going to mean this business is going to stay stronger, because I think he gets that this is not about just milking the market to make a ton of money right now. And if I have that kind of a model, I’m going to have great earnings and a few great quarters, but I might blow up. And then when the markets go against us, things aren’t going to it’s like, it’s like investing in meme stocks as opposed to good value.

Jamie gets good, remember, if I remember correctly from the book that I read, him and Sanford Wheel were all about the balance sheet. Sanford Wheel to him was like, that’s the balance sheet. It’s about the balance sheet so that you can withstand anything.

And when you have that asset and things turned down, you’re now in a position to do exactly what he did with SVB because you have that balance. Exactly. Exactly.

It’s a fortress balance sheet. And that says a lot. It says a lot that they have weathered all the stuff that they were prudent along the way.

They weren’t just trying to make a quick buck and that’s going to really matter in the long term. And gosh, the stock is still this cheap. We just keep it on the focus list and just keep reiterating.

It’s a great place, I think, to put some money in a risky market. So the risk reward here is the right place. A safe harbor.

So obviously we’re just starting earnings season now. We’re basically kicking off week number two again, just throwing it out there, not prep on this particular topic, but I know you do a lot of interviews. Any stocks coming up with earnings that you’re like? Yeah, that’s one I’d keep an eye on.

We were just looking at one. We like a lot of these basic material stocks, Pete. I think we’ve given out some really great ideas previously with respect to New Corp, steel Dynamics, Warrior, Met Coal, and some energy stocks.

We like energy. We think we’re going to see a big return to energy, financials, basic materials, and just because these are the things that have been overlooked in favor of the sexy AI and everything else. And those stocks are overvalued.

These stocks are undervalued. And I think we’re sort of think the Fed is trying to very slowly wean people off this speculative, risky behavior because it’s ultimately bad for society. We actually just yesterday called out CF in basic materials.

We’re actually seeing the same thing in sector rotation. Just basically broke a much longer term move to the downside, consolidated into accumulation for the better part of, gosh, a couple of probably about three or four months. Let me actually just I’ll share the screen here for 1 second.

We can work our way through the swing trade that we call that. This is our daily newsletter that we put out every day to our members. And this is actually what we were looking at in CF.

Finally broke much longer term order flow to the downside. And the pick that we actually had, believe it or not, 74, 80 was the buy stop. And we always incorporate an edge share price and CF actually hit the edge share price just in two days.

And you can see actually the 87 80 level is what we’re looking for. So I love when stocks break these longer term moves. You can actually see here, it didn’t invalidate this move to the downside.

Finally enough time went by and looks like we’re sitting actually in a pretty decent spot right now. We already added once, waiting for it to get up to that 88 area to look for another position. Yeah, CF gets a very attractive rating in our system and its price to economic book value is 0.3,

which suggests from a fundamental perspective, there’s a lot of upside. So good technically and fundamentally, we’re looking at some of the same ideas. And we’ve been watching the energy sector.

I think we had 14 stocks yesterday that met what we called a stacked order flow criteria. And EOG and a couple of those we were looking at, EOG, I think was at the top of our list. And SLB, Slumberger actually has had an amazing couple of weeks.

We’re waiting for that to slow down a little bit to reset what we call the optimal entry. Yeah, I got a small team, but sometimes we look at some of these sectors, I’m like, we can’t get enough of these ideas going. Man, EOG looks attractive too.

I mean, it’s a price to economic book value of 0.6. So price is implying a permanent 40% decline in profits. Okay, so we got a bunch of new ideas on top of the ones that just reported.

So what we will do is we’ll put a nice summary below the description in the video. And if anybody has any follow up questions, absolutely, leave them in the comments below. And David.

And I will both leave some links down there as well so you can get a little more information as well. So, David, as usual, thank you so much. Really appreciate your time and I will speak to you soon.

Great. Thank you, Pete. My pleasure.

Take care.

Responses