The Daily Ticker Podcast Expectations Investing

Transcript

Hey, everybody, it’s Pete. Welcome to today’s episode of The Daily Podcast. Today we are here with David Trainer again from New Constructs.

How are you, David? I’m doing great. Good to see you, David. The market took a little bit of a beating today.

I’m going to show you how I spoke about this yesterday and why I kind of saw it coming. We’re going to tie a little bit back into baseball. We’re also going to talk about two books I want to show everybody today.

But looks like you had a little bit of a beating recently as well. What’s going on? Good work. Just Pete’s not beating me up.

Jiu jitsu class today, I got a little bit of a shiner. It looks a lot worse than it is. It makes you look tougher.

It makes you look tougher. You’re looking good. Thank you.

Thank you. I try to yeah, it’s it’s yeah, we were doing some special some weird chokes today, and I think one of the geese scratched me, so I didn’t get punched or anything cool like that. It’s more like a rug burn.

Not very exciting. All right, so David, toughening up. A lot of traders, investors are going to need to toughen up.

So we’re going to give you some insights today. Big thing we’re going to talk about today is, could you have seen the selling that happened in the market? We’re actually going to take a look at that. So it’s in the video.

I want to show you something I wrote yesterday and why I saw it coming in the market, which is actually going to bring me into something else, which we get a lot of questions and feedback either on the podcast or on YouTube asking about how do you rectify the difference between long term fundamental outlook from actually timing into and out of trades? And it’s kind of what’s different about what David and I do in the same arena. So I want to suggest two books that I want to bring up to everybody. Something that from the library in the back.

I give friends a library card when they come over. The first one’s on the fundamental side. And this is actually a book that David had suggested to me a while back, expectations Investing.

And actually, David, I didn’t tell you this, but Michael Malbusan, if I’m saying that correctly, I don’t know how I think it was somebody on Twitter or something like last week, somebody on Twitter downloaded every single report that he’s written in, like, the last 20 years. It’s a 1200 page PDF. So I was telling you before I actually went away last weekend, and I read most of the 1200 pages from my hotel room.

So very interesting. So, Expectations Investing, I’m going to give you a little bit of feedback from what I got out of the book. And probably one of the biggest things that David has taught me is when you think about a company and their earnings.

And we all know that the guidance will pay for the cash flow going forward. But longer term thinking is when a company has a product or a service, that is kind of their reason that you want to invest in the company, whatever that hot thing happens to be at that moment. Most of those companies have what’s known as a growth appreciation period.

And David talks about that all the time. I went into a little more detail in that particular book. So if I can give you an example of Amazon, who has earnings this week as well, scheduled earnings this week had obviously their core business, right? And that was their growth appreciation period for a certain amount of time.

And you were investing in those earnings. And then they came out with Amazon Web Services, which is where a lot of their net profitability came from. And then they had another growth appreciation period on top of that.

So that kind of thing fascinates you, where you’re now looking at headlines for a company and whether or not they have the next thing coming out for you to invest in the future. That book, I’ll bring it up here one more time. That book is fascinating.

It does a great job. I think the original one, just to really date the book, the first version of it that I bought, the examples that they used was Gateway Computer, which not even around anymore, but big popular company with their cow covered boxes back in the day. The new version, they have a big breakdown on Domino’s Pizza.

So they kind of updated a little bit, bringing it into the second part. Actually, you want to touch on that a little, David, because that’s really more your arena, that book or that particular topic. Yeah, no, I think expectations investing is the absolute most intelligent way to approach valuation from a fundamental perspective.

The whole idea is that rather than be a fortune teller and try to predict stock prices, why not be a critic of Mr. Market, who has to be a fortune teller and criticize whether or not the expectations embedded in stock prices are too high or too low? And we have actually built, I think, the best ever platform for investors to apply the expectations investing concepts. Mobison and Al Rappaport are people I started my career working with.

Mobison was my first boss and mentor on Wall Street, and I built a model based on his original ideas around expectations investing. We use that all across Credit Suisse and with new constructs. Effectively, I’ve scaled that up.

And it is true to all these concepts, all the concepts that were written about in Al Rappaport’s creating shareholder value. So we’re big believers in all that. Mobison is really wonderful financial writer.

He’s kind of almost like a Michael Lewis in finance. I mean, he makes it somewhat interesting and it’s easy to read. It makes it very relatable.

You can understand what he’s talking about without getting into the spreadsheets. I mean, you could do that afterwards, but he makes you interested in the topic. He does a great job.

It was really one of the great joys and pleasures of my life to work with him. He was an amazing mentor, great speaker and all that, really. Gosh, I learned so much.

It was amazing. And then I basically started New Constructs to implement all the concepts that he and I worked on together and talked about and that he’s been a thought leader in for decades. We 100% are subscribers and believers in what Mobison and Rappaport have been saying for 25 years.

And New Constructs is, I think, the best ever implementation of that so that everybody can take what they read in those books and make use of it. And I’m going to show you four examples of that today. So it’s pretty exciting.

So the second book I want to talk about, which is a little bit more on my side of the business, which is a little bit more short term in nature. And by the way, we’ll put links to everything we’re talking about today in the show notes, including that 1200 page document. I got to find the Twitter link where I found it.

The other book is this one right here, studies and Tape Reading by Richard Wykoff. Richard Wykoff is widely known as the father of technical Analysis at the turn of the century with Jesse Livermore and Bernard Baruch back then to a little bit lesser degree, Gerald Bloe, kind of the turn of the century, all the chart patterns everybody’s known for today. So this is where we kind of bring together the fundamental reasons to look at a stock, the future, cash flows, and then timing in and out of those.

So these two books have heavily influenced me, especially this one on the short term side of things. In the footnotes, we’ll put links to Amazon for both of those books, including that link to Twitter for that 1200 page download in case anybody really wants to bury themselves in that. So I want to touch on just briefly, David, if you don’t mind.

I’m going to share the screen here for a second and I’m going to put up this is actually what unfolded in the market today. And you can actually see even the large caps took a hit today, what we’re calling the Magnificent Seven. Not actually following through today.

Look, it was kind of overdue, let’s just face it. I mean, when things are going straight up for a while, you got to breathe a little bit. But I want to talk about two things.

Number one, I want to talk about is it possible to see this happen before it happened? And I want to just bring everybody into what I wrote in our private letter, in our private research yesterday here. And you can actually see, this is from yesterday’s, so I’m not pulling this up after the fact. I don’t want to spook the no hitter again, to use a baseball analogy, but we’re seeing many second tier stocks get order flow, and that’s very significant.

The leaders are running out of room to justify the new lofty levels, which is something that david’s been saying for a while now, is where they are now are not justifying going up higher. So it’s not a question of whether or not a lot of these stocks were still bullish. It was a question of whether or not they still had room to go.

So what we also do, again, in the research, part of what we do is I run this proprietary scan, which is 20 day highs versus 20 day lows, and the difference between those. So this is what we’re talking about here, and you can clearly see that there’s a decrease while the market was still kind of working its way a little bit higher. So these kinds of clues are where the tape reading kind of puts itself in the context of the longer term picture.

And again, being very clear, everything we’re talking about here is for educational purposes. We’re not telling anybody what to do. We’re telling you how we’re seeing things and how we’re doing it.

And what we started to see and what we started to put out in our research yesterday before this happened, before the downgrade for the United States today, we started to see that we were seeing second tier stocks start to rally. Not the nvidias and other stuff, all the stuff that’s probably like in the garbage heap. And again, using that in context of what we’re talking about, that when they run out of room on the leaders, they have to start putting that capital to work.

And you start to see these other ones rallying while the leaders are coming down. And we saw that microsoft starting to take a hit. Tesla.

If I could just show the screen one more time really quickly. We did a big breakdown on tesla and this longer term move and literally kissed the level that we’re watching in tesla. It’s a little bit below that level.

The 253 level is basically what we’re talking about. When you start to see these clues adding up, it doesn’t mean the whole order flow or the tape is changing, but it means you need to sit up in your seat and say that something is happening. You now need to get in there, because the whole thing is not going in one direction as it was.

We had 13 days, I think 13 out of 14 in the dow where we were positive. It’s got to cool off a little bit. It’s not a bad thing.

It’s actually okay, because in our universe, we’re resetting the optimal entry for a new move in that direction. And this is perfectly fine. You just need to be on top of the trade management.

If you know your objective, if you’re looking to hold it for a week, you got to sit up and maybe make a decision. If you’re looking to hold it for the next year, this is maybe even a better spot to add to the existing winner. So everybody’s got different objectives.

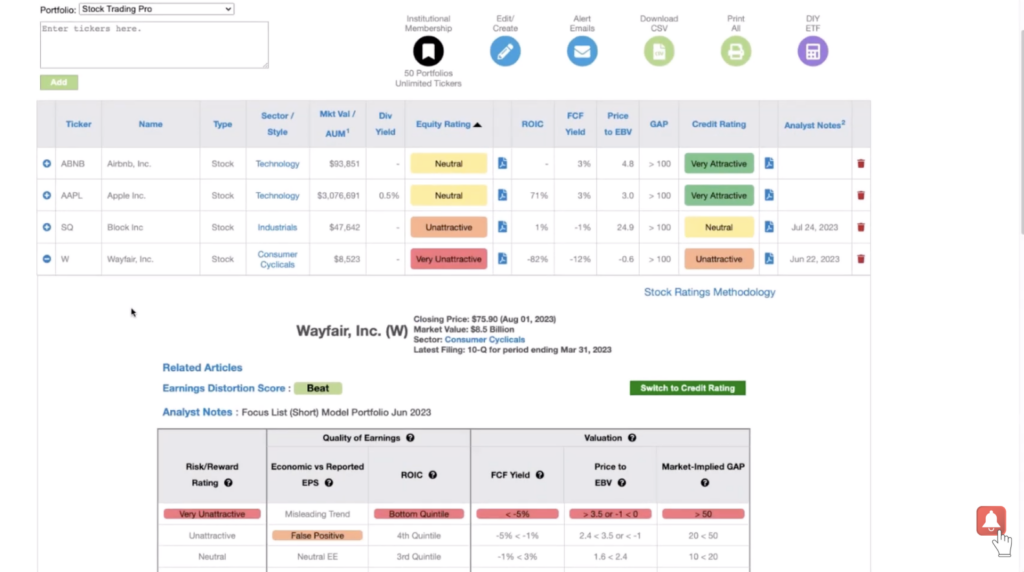

So just wanted to get out there. So I think what we’re going to do now, David, we have four stocks. I thought it would be really kind of fun if we dug a little bit deeper into earnings that were coming up.

Looking at them through the lens of new constructs and how they do it. We’re going to talk about wayfair apple sq. I keep calling it square, but it’s block inc these days and airbnb.

So Dave, you want to take the screen, do a little bit of context on what you’re looking at. And again, just so everybody understands, this is where you have the wind in back of your process. I just want to give a little context.

We do a lot of one on one coaching in our community and one of the biggest problems by a mile. Once you understand what to look at, it’s not that hard to find stocks that have stacked order flow and you could kind of time your entry. It’s understanding and earning the conviction to hold your good trades longer that makes the difference between you made 10% versus you made 35% or more because you weren’t influenced by the minor fluctuations back and forth.

You actually had a reason to be in that stock in the first place. And those are the kind of things that David’s going to introduce you to right now. A little bit different longer term take having a reason of what’s likely to happen for a company? Not definitely.

Again, this is all education, you have to make your own decisions. But what’s likely to happen based on the cash flows of the company, the historical cash flows of the company, and what that means now, justified by today’s price. So David, I hope I didn’t take too much of your thunder.

It’s on you right now. I got so much thunder, you could never take it all. And I don’t know if we’ll be able to get through all of these stocks because the work that we do is sophisticated.

That’s part of why I built the platform to implement all the stuff that I learned from Mobusin and Rappaport. Because doing it manually for even a couple of stocks was extremely difficult and time consuming. Even as an expert pioneering the development of these models, I got fast, but the most I could ever work on at any one point in time or have under my own coverage when I was a traditional analyst on Wall Street, gosh, maybe half a dozen.

So having a system that does this for 3000 plus stocks, eventually all stocks in the world I think is powerful. So going through quickly on kind of looking at the risk reward, and to piggyback on what Pete has said, it’s all about risk reward. I’m not telling you what you need to do.

I’ll never tell you what you need to do. I don’t know you. I don’t know what you need.

What I can tell you is the math. The math driven, logic driven narrative that we use at New Constructs. And by narrative, I’m trying to draw a very clear distinction between the theme and story narratives that we see on Wall Street and on Kramer and all these guys.

It’s all about talking about, oh, hey, Kava is the next Subway or beyond meat is the next whatever. We don’t do that. Those are not our narratives.

Our narratives are math and logic driven. And that starts with green is good and red is bad. So if we’re looking at the screen and we got the four stocks that Pete mentioned before, and we got an equity rating and we have a credit rating, red is bad, green is good, and I’ll talk about and neutral is somewhere in between.

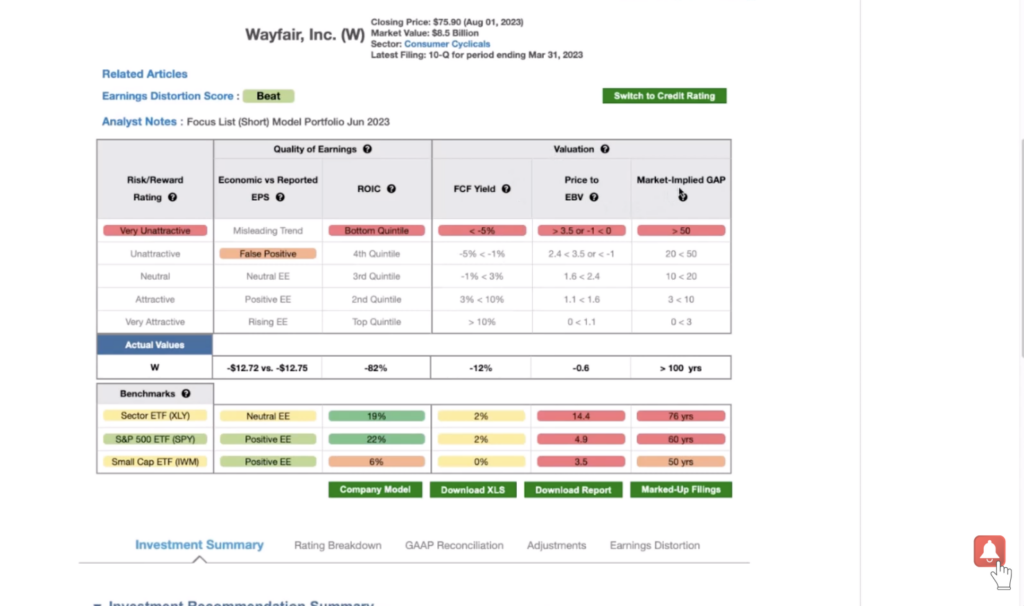

Right? So let’s start with Wayfair, because I believe it’s on our focus list. Short. It’s been ripping lately.

Our team has been kind of begging me to talk about it because they’re like, this is just nuts. The expectations baked into the stock price are really pretty outrageous. You see that here on the right hand side? Pete mentioned before the growth appreciation period.

Mobusin calls it the competitive advantage period. It’s the same exact concept. I didn’t want to copy his name, so I used a different one.

But the idea here is just that the expectations baked into Wayfair are super high. So you can see, yeah, it’s a zombie stock. If we look at the report we wrote on this, you’ll see that we do this really cool analysis.

I think it’s cool talking about ourselves here. Of course it’s a zombie stock because it’s burning cash, and it only has eleven months. At the time of writing, they had eleven months of cash on the books to sustain the existing burn rate.

Right. That was back in October. So things have hopefully something’s going something’s got to change there.

They got a lot of competition, but let’s talk valuation expectations baked into the stock price. All right, so let’s start with Justifying. At the time, the price was $42 a share.

Our model shows that Wayfair would have to immediately improve its margin pretax margin to 3%, and grow revenue by 15% compounded annually for the next eight years. In that scenario, the revenue would reach 48 billion, or 2.4 times the combined trailing twelve months revenue of Ebay Williams Sonoma and Overstock.

That’s a big number. Wow. That’s what they got to do to Justify.

$42. And then at 3%, Wayfair’s pretax profit margin would be higher than Amazon’s North American non AWS operating margin of 2.6%. And even that’s fallen recently and greater than Wayfair’s best ever margin of 2.9%

during COVID It also shows that their profits would go from negative 943,000,000 in the last twelve months to 1.1 billion in 2030, which is 2.9 times better than they’ve ever done and 11.2

times what their peer haverty has achieved. David, can we just stop there for just 1 second? I always like to bring it back to what does that mean? First of all, those numbers are when the stock was at 40 and change. $40 and change.

That’s, right. So right now, as of this moment, which is August 2, 2023, the stock in the last 46 trading days has gone up 110%. So it’s nearly doubled off of those projections.

So if those numbers didn’t make sense at 42, think again, educational purposes, what does that mean? Where the stock has gone up 100% and it didn’t justify the risk at 42. Right now, as of the close, it’s 72. Again, all of this is about what’s likely to happen, not what’s definitely going to happen.

That’s a monster mistake that people make, what’s likely to happen. And then you throw in the numbers of the other companies, and it would have to dwarf what the other companies are doing. So again, just really think through what’s the right price to justify what’s likely to happen next? That’s really the big thing we want to get across.

I think it’s really good to double tap on that. Pete that’s a really clear thing. Look, what Mobison starts with in expectations investing is that investing is about buying low expectations, selling high expectations.

Buy stocks with low expectations, lower than your expectations. That’s why we can’t really ever give advice, because I don’t know what your expectations are. But if the market’s prices, expectations for future cash flows are lower than what you think the company is going to do, then that’s a potential buy for you.

If they’re higher than what you think the company is going to do, that’s a sell. Right. So in order to know whether or not your expectations are higher or lower than the market, you got to quantify the expectations baked into the market price.

And you also have to have a pretty good reason for that expectation, which Warren Buffett talks a lot about. What is your circle of competency? Other than the fact that it hit a scan and went up last week? No, exactly. Yeah.

Right. Kind of goes without saying. Expectations got to be somewhat reasonable.

So we’re looking at $45 or $42. Right. And then just see how much downside there is in this stock.

If you’re looking at more reasonable growth rates, a 50% compounded annual growth rate, that’s a huge number. I think the revenue growth of the last few years has been negative. Pete and so if we assume a different scenario, this is what we always kind of do in our research.

We’re like, all right, this is what’s going to take to justify the current stock price. This is what’s going to take to justify another price. Well, in this case, it’s one dollars if the notepad margin goes to 2.6,

which is equal to Amazon. And by the way, I think at this time that the margin was negative for Wayfair. So going from negative to 2.6,

that’s a big jump. Yeah, you can see Wayfair negative 8%, a negative 71% return on capital. So going from negative eight to positive 2.6,

like this year, and then grows a consensus, which was negative twelve, one and 11%, way below the 15 compounded annual we gave them. And then we say, okay, after that, they’ll just keep doing 10% way above normal retail rates. Right.

So, hey, we’re giving them a good credit here. What does it mean if they do that? The stock would be worth just $1 if they do that. Wow.

Right. And so let’s take a look at what’s implied by the current stock price. I put together in our Model a scenario here.

I’m going to call it optimistic. And we got a neutral as well. And you can see the historical revenue growth super high in 2020.

That was a COVID year. I think people stocked up pretty well in furniture. And so we’ve seen negative year over year.

I think 2023 is supposed to be negative, bounces back to 813. Eleven. I went ahead and put twelve in here at the optimistic, and I ran twelve out for 25 years just to see what would happen.

Right. And then here’s that 3% pretax profit margin. Right.

The TTM at the time of our report was negative eight. Looks like it’s gotten worse since we’ve gotten a few more queues in. Now it’s a negative ten.

So we’re talking a dramatic and immediate improvement in profit margins. Dramatic, right. While also eventually growing at high rates.

What does that mean? So let’s take a look. Here’s my optimistic scenario that I showed you before, where the margin goes to 3% and they end up growing 12% compounded annually for 25 years. That puts us out here in like 2047, 2048.

You can see the implied values go way high real fast and then it flattens out. But we still can’t get to $75 a share. You see that’s up here, 70.

The best we’re really getting to here is in the 53, maybe $60 a share. And that’s ensuming 100 years of growth at 5% compounded annual. Again, in this time frame, it’s that 12% that I put into the model, plus the three years of different numbers for consensus.

Right. And that much higher margin. The return on invested capital will, on average, in that 100 years be at 417%.

I mean, in 5% compounded annually for 100 years, that’s a pretty good rate for a retail company. Anyway, you get the idea. Those are the expectations baked into the stock price for Wayfair, according to our model.

And I just want to keep touching on this topic because it’s definitely one of the things that, in my experience, a lot of people come into our community have wrong. It’s the wrong context for what it means to be a speculator, whether it’s actively trading whatever that objective means to you or whether it’s being an intelligent, longer term investor. It’s about what’s likely to happen when you’re about to hit that button to get involved.

And we talk about this a lot. You have all of these decisions and all the information up to that moment you’re about to make that decision based on however you built that argument. And David just went through optimistic and what wayfair has done.

We’re not saying anything about the company. We’re talking about what’s likely to happen at a certain price based on what the stock is saying historically, it’s done. Then you have a new set of decisions after you buy that, and again, that growth appreciation period of what’s likely the cash flow that you’re buying going forward and what the stock and the company needs to do.

And we just talked about going from negative to two and a half times. That’s a big jump for a company to make. And then you got to start taking into consideration, are we in inflation, recession, competition? All of those other things.

So these are little things that you need to really say, what’s the argument for me deciding to hit that buy button? That’s exactly right. I love it, Pete. I mean, you’ve got to have a good argument from a fundamental perspective about the realistic future of the business.

How does that compare to what the stock price implies? And then that’s your fundamental process. And then otherwise you’re kind of speculating or using other strategies based on reading tapes and things like what you do or reading DTA and that’s fine, but from a fundamental perspective, yeah, you absolutely have to have some kind of thesis that says, oh, this is why I believe. So I did another scenario while we were talking, Pete, and so it turns out, to justify 75 90, the company’s got to grow at 16%, compounded annually for 15 years, while improving their return on invested capital from negative almost 100% and average 60% over the whole time frame.

We can actually go look and see what the implied return on invested capital is by year 15 because over this time, the return on capital is going up. We can actually look, it’s not one of my favorite charts because it’s a little bit harder because you got so much future stuff in here. But you can see here’s where the return on capital has been in the past.

Look at the scale on this thing. Goes up to 1100%, but the implied return on invested capital in year 15 of the model is 156%. So return invested capital is going to go from negative 100 effectively around here, right.

To 150, while also growing at 16% compounded annually. I got a hard time believing that the company would ever do that. Those are flying tech stock returns, not somebody selling wicker furniture.

Yeah. In my opinion, yes, that’s a really amazing business performance for a tech stock. Absolutely.

For any company. But, yes, that’s something you could only it would be very difficult to believe that would happen in anything other than some sort of tech stock. Yeah.

Again. I want to keep bringing it back to what I’m actually good at is you have to really think before you can hit that buy button what’s likely to happen based on all the information you have. And all David’s doing now is going over the numbers of what is likely to happen.

And then everybody makes their own decision from there. Do you think it’s likely those best case scenario projections are going to happen or what the stock has historically done is likely? That’s really where the longer term investment discussion starts. So let’s hop on to the next one.

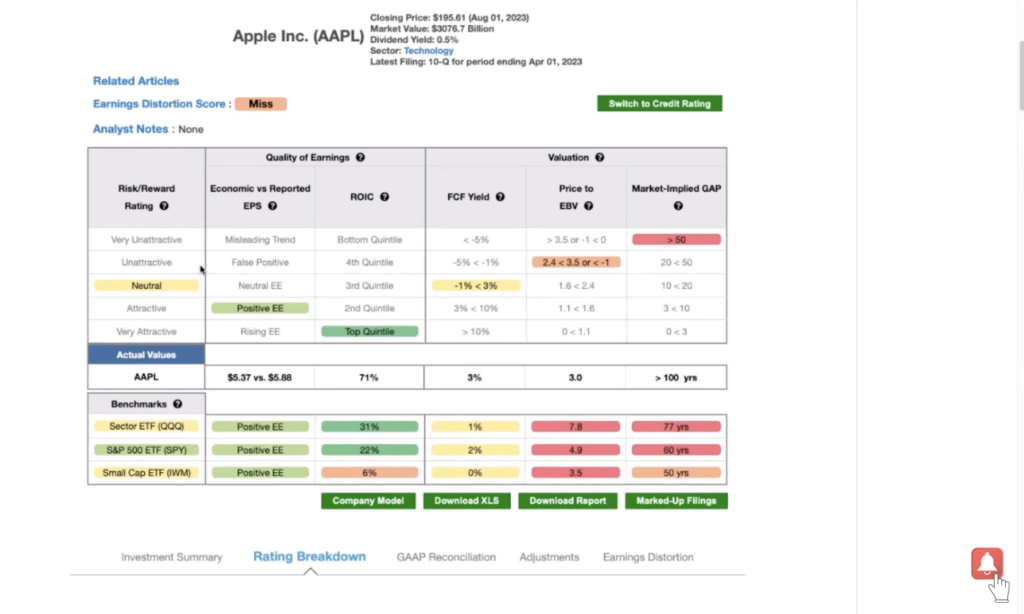

What do you got next, David? Yeah, let’s take a look at Apple, because its valuation has in the past been much more tame, but it’s a neutral rating now. And, yeah, I’m seeing a little more red here than I expected, Pete, mainly because returns on invested capital for Apple have been amazing. Right.

But as a tribute to sort of the law of competition, we’ve seen the return on invested capital for Apple come way down. I mean, it was 300% at one point, Pete, for a few years, and it was, look, just going back five years, 143%, and it’s 106, and now we’re down in the right. It’s difficult to maintain really high returns on capital.

Kind of give you some context on Wayfair, like, oh, so Wayfair is going to have a higher double the return on capital that Apple is able to achieve. Again, is that likely? Probably not such a good conversation to have, like, even just hanging out and thinking about it from a common sense perspective. Yeah, absolutely.

That’s the beautiful thing about these kinds of logic and math driven narratives or discussions. It is common sense. It is common sense.

That’s what I like to feel like I’m bringing to folks, is all the noise and hyperbole out there. Common sense on. Hey, man.

Do you think from a fundamental perspective, is this likely to happen or not likely to happen? I think something that you do specifically, David, is you’re bringing the complex processes that probably a lot of people don’t even want to do, and your software is putting it into a report that makes it easier to at least have an informed decision. I love that about the new construct software. Thanks, Pete.

That’s the goal. I mean, that’s another book that Mobison put me on early on called Consilience. And the whole idea is that the value we add in a digital world in an information age is.

Synthesizing lots of information for our clients and for our peers. I think also too, is because there’s so much information. What information? You’re looking at matters.

And you and I actually we’ve been talking there’s the four steps, the Value Investing 2.0. We’ll put a link underneath for everybody to look at that as well, but knowing what to look for, one of the things that we talk about in our universe is when you know what you’re looking for, you’re never lost. And most people never get to that point where they’re saying, that’s the only thing I’m looking for.

That’s what matters to me. And we have a very specific way of doing that in my universe. And you have the four steps for Value Investing 2.0.

So I think that’s a big thing to bring out here too, is what you’re looking for matters because everybody tries to put all of that too much information, quite honestly, and that’s why the market becomes overwhelming, because you’re trying to look at everything as opposed to something that matters to help you make an informed decision. And you just saw that on David’s screen. We’ll go over that, I guess, now in Apple, Dave, maybe a little deeper.

I mean, thank you. That’s like the ultimate compliment, Pete, because that has been our goal, is to really simplify things for folks, because you’re absolutely right. I mean, you want to look at just one filing for one company.

You’re talking about 200 to 300 page document. I mean, that’s a lot. The mirroring effect always throws me off there.

But yeah, it’s a lot of work, right? I mean, then there’s all this stuff that’s coming out in the news, blah, blah, blah. We boil it down to green is good and red is bad, and you can go into as much detail as you want. Apple is a pretty great example of good company, not so good stock, right? That’s the green here.

They got positive economic earnings, a really high return on invested capital, but not necessarily good stock because you’ve got some pretty high expectations baked into the stock price. So David, it’s interesting to bring that back to what we talked about before, the growth appreciation period. We gave you Amazon as an example.

So now, again, just to keep it common sense amongst friends, right, what would be the next reason Apple would justify being at all time highs right now? Buying it right now and saying what would be the next thing that would catapult it to another growth appreciation period? That justifies new all time highs and beyond. Not just buying it at this particular moment, but and beyond, what would be the next catalyst? And I personally think the easiest way to really think about is Amazon sold books and then the Amazon web seller AWS Web Services, became the next catalyst. So if we’re looking at Apple, which is scheduled to report this week as well, what would be the next catalyst? What would be the next opportunity that you believe where the future cash flows other than their existing balance sheet? You’re not buying what they did.

You’re buying what they’re going to do or what the outlook would say. Those are things you need to think through. And that’s why David made a very big distinction between a stock versus a very, very big difference.

Yeah, one of the things that Mobison really blew my mind with early on was he wrote a piece on competitive advantage period, like, one of the best pieces ever. And I actually literally went around the entire Credit Suisse Equity Research Department and gave a copy to all these people. Like, you got to read this, because what he points out is that growth appreciation period as a concept, links strategy, which is what you’re talking about, Pete, strategy to valuation, right? So if you see these super high expectations baked into a stock price, you have to ask yourself, what is the company’s strategy to meet or beat those expectations? And so what’s really cool about this kind of discounted, this concept of growth appreciation period, is that you’re really able to explicitly quantify what the cash flow lifecycle has to be to justify the stock price over the rest of its life.

And so that makes you say, okay, well, if they’re going to do that, what does the business have to do to generate those kinds of cash? And to your point, Pete, it’s like, all right, so what is Apple going to get into next? They got phones, they got watches. What’s it going to be? Is it going to be drones? Is it going to be self driving cars? Is it going to be other wearable devices? The big one they talked about now is the new virtual reality stuff, but that’s more hardware we’ll see. That’s the investment part.

What do you think? How that’s going to affect buying Apple now at or near all time highs? How do you personally think how do you build that argument to justify that? That’s right. And that’s strategic analysis. That’s porter’s five forces, right? Because you can’t just say, oh, well, they’re going to build a super great headset.

Well, guess what? Other people are building great headsets. And by the way, you start making a lot of money on a headset, you’re going to invite a lot of competition. And why have Apple’s returns on capital dropped from 300 to 150 to 70? Competition people don’t let you just go make a lot of money, like, oh, Pete’s making 50% margin on that.

You know what? I bet new contracts can do it with a 45% margin. And Pete says, oh, I’m going to drop to 40. I go, I go 35.

Right? That’s a race. Race to the bottom. Exactly.

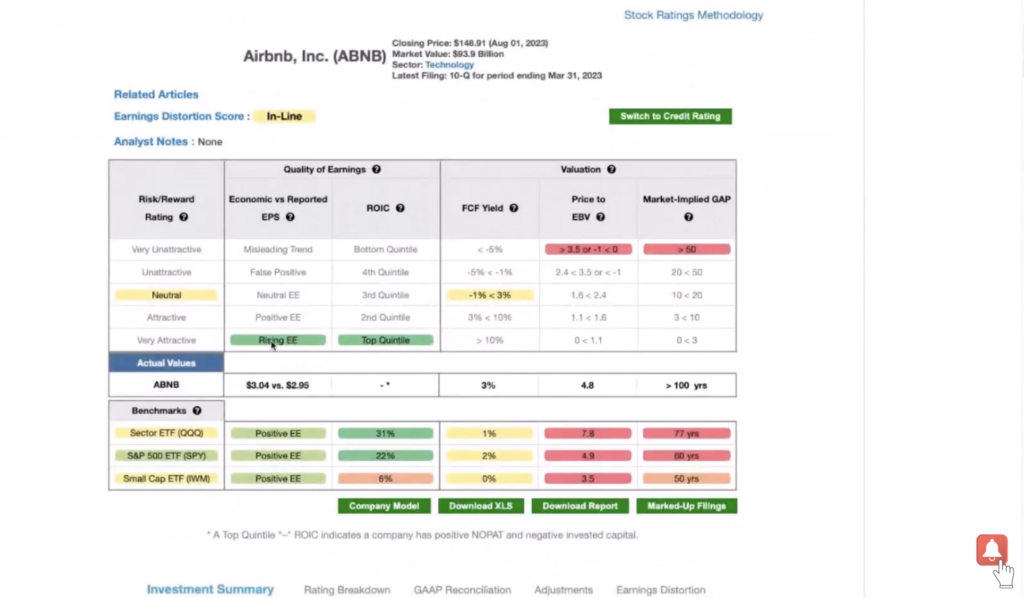

So let’s talk about airbnb. So let’s see you go to expand the rating here, it’s got a neutral rating, okay? That’s because you got pretty good economics. And it’s a really high return on capital.

They got a negative invested capital. That’s what this is showing here. But valuation is high, real high.

Let’s talk about that. I got the model open here, and I did a couple of scenarios. What we’re showing for Airbnb is it’s got to grow revenue compounded annually in this optimistic scenario at 11% for 30 years.

Wow, that’s a big number. That’s a long time for double digit growth. And it’s like, okay, so what hotel has ever grown? Right? Tell me what kind of innovation Airbnb has to bring to the table in order to maintain that kind of growth while also, again, continually improving return on invested capital.

What do we have for return on capital? That’s interesting. Gets super high here, then it drops down later. Let’s take a deeper dive on what’s going on there.

The one benefit that they have is people are starting to get out of the house a little bit more now. So you have to think, how long would that affect? So there’s total addressable market, which is how many people are traveling. That has obviously changed a little bit.

We’ve seen that a lot with the airline stocks this year. Even the cruise lines. Royal Caribbean NCL took a little bit of a hit.

But Delta United, Royal Caribbean Norwegian Cruise Line had a phenomenal last three months. But that was everybody booking into the summer, and oil prices were low. Now oil prices are going up.

Everybody’s booked for the summer. Kind of the same thing with Airbnb. What are you looking at going so, yeah, the invested capital numbers for Airbnb are super low.

That’s why the return on invested capital gets funny, because you got a really small denominator. So we actually show no return on capital here because the invested capital is negative and I think eventually gets positive. It goes super positive like I showed before, because they just start to have capital.

That’s why that chart looks so funny. And then as the capital base builds up from negative to positive, you see a big number here, but the free cash flow numbers just continue to be huge. So we’re talking about Airbnb generating 345678, 910, 15, 2030, whatever, 35.

And then in year 30, we’re looking at generating almost 40 billion a year in free cash flow to get to this 148 plus stock price per share. And that’s also with the revenue growth of the Kegr is going to show right here that’s that 10.9% that I showed you before.

So you don’t actually even get a return on capital because we’re assuming that this business is able to operate with negative invested capital for 30 years, which is ridiculous. That’s hard to do. Amazon did it early on in its days, doesn’t do that anymore.

And there was a lot of pushback on that. It was 20 years. And we’re going to make profits soon.

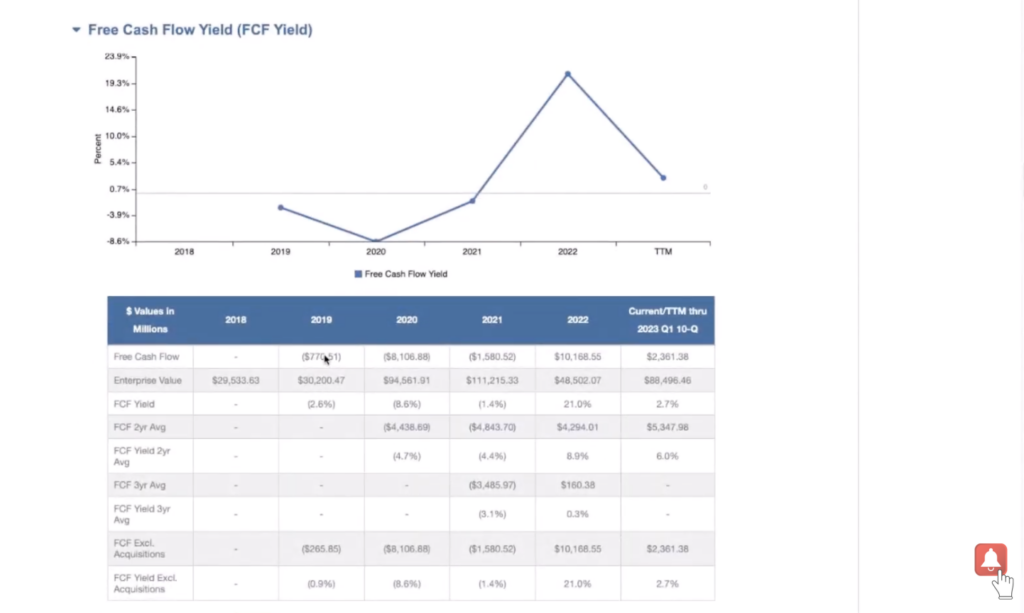

Yes. And so, yeah, I think this is a great example. Pete, to your point, what is it that Airbnb is going to do in order to be generating 40 billion a year in free cash flow in 30 years? If we go to the rating breakdown page on Airbnb, I’m curious about what their free cash flow has been in the past, because they got to get to 40 billion a year.

It’s been negative 800 billion, negative 8 billion, negative 1.5 billion, positive ten and positive 2.4. So that’s a rather large improvement in annual free cash flow generation.

That, again, I think this is a return to travel kind of bump year. This may be more normal. The point is, what could Airbnb do? Could they maybe create something that automatically cleans all the houses? Well, that’s the thing, is can they get more people? You got to think about different ways that they could increase the revenue, get more people.

Well, maybe that’s being helped a little bit. Where this summer it seems like we were talking about before the cruise lines and airlines, but that’s already baked in. What kind of more inventory can they possibly have? So let’s say we get back to normal.

Can they increase their inventory? They’d have to increase their prices for what they do. Then if they’re increasing their prices, are they really differentiating themselves? Might just go to Marriott or Hilton or something along those lines if it doesn’t make sense anymore. So prices is probably they’re not going to increase the total addressable market.

It’s got to be prices. It’s not their own inventory. It’s other people’s houses.

So that’s something to keep an eye on. With the price of Airbnb, again, port of five forces, how can they increase to hit those numbers? You’re talking about the opportunistic part. It’s not like the hotels are not going to respond, of course.

And by the way, the hotels would love it. The amount that Airbnb would have to raise prices and fees to get to these cash flow numbers would be so much that it would put them out of business. It’s super interesting, the emotional part of a hot stock market for a period of time and then whether or not that price it just got pushed up to makes sense to get involved at that price.

I want to keep going back to that because it’s such a big part of my community. Whether it’s a short term trade or something, we’re holding on from one quarter to the next. It all comes down to what’s likely to happen next for the risk that you have to take.

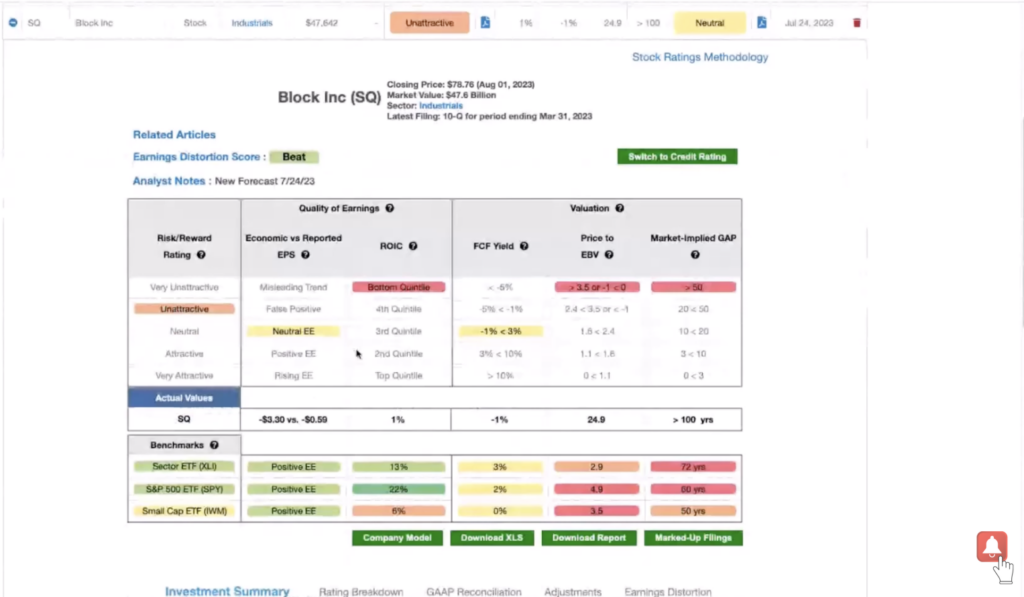

And Dave is just doing a little bit longer term picture based on the numbers of what the company normally does and then reverse engineering it back to the current stock price and whether or not that’s likely to continue. That’s a fascinating we could we could go forever on this. We got one more do we have time for one more did we cover all four sq? Sq.

Let’s go take a look at how bad sq is unattractive. Pete, you gave me a list of really expensive stocks today. Well, it was actually earnings that are coming up.

That was the list. Okay. That’s where it comes from.

Yeah. So this gets unattractive rating because it doesn’t even have necessarily looked like a good company, but definitely looks like an expensive stock. It is not on our not on our zombie stock list.

So I’m guessing the free cash flow isn’t too bad. I did open a model here to look at some implied levels of performance, and so I got a neutral scenario here we created where it looks like to justify the current stock price. Interesting, I did this back in August of 2020.

It’s still sort of relevant, but they got to grow revenue at 18.5% compounded annually for 23 years while improving their return on invested capital spread. Return on invested capital versus cost of capital spread to a high enough level that it averages 7.6

over 23 years. Looking at where the company’s been in the past, that looks like a pretty big ask. That means they got to raise prices a lot.

They got to really improve their margins and then grow revenue at nearly 20% compounded annually for 23 years. Again, what are they going to do? I got an idea when if you gave me a microchip that I could put under my watch and when I tap like this, I could pay for something. It’s like a baseball signal.

You got to go to the hat first. And the left elbow and the right elbow. 50% tip, 20% tip.

So I guess one question that I think I would be thinking if I was watching this or listening to this, David, is how do you come up with the growth appreciation period? Because we’re talking about sometimes it’s ten years, 15 years, 25 years. And I guess we’re talking about how the current stock price, justifies how many years out, right. Is that basically we’re talking I’ll show I’ll show it to you.

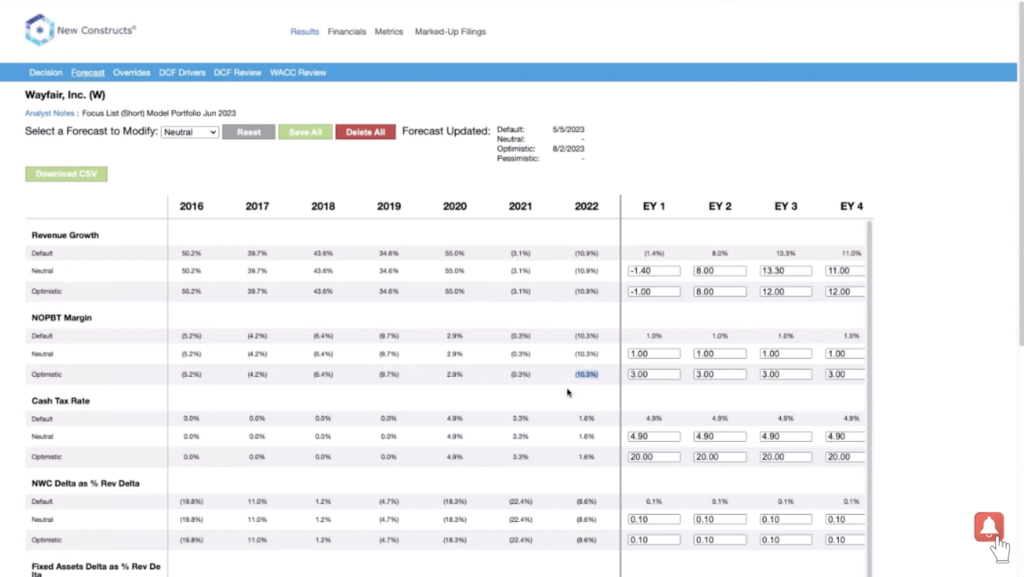

So if we’re looking at this square know, look, everything Pete starts with green is bad and green is good and red is bad, because I want to synthesize, I want to give people something they can roll with. But we will go into as much detail as, you know, Pete, to show people how we get there. So what I’m going to show you is under the hood on the discounted cash flow model, how that works.

First of all, you’ve got to have your set of forecasts in here. And so you can see for the optimistic scenario, we put these numbers in going out quite a ways, and the neutral scenario, right. And there’s the improvement in the margins.

You can see the best ever margin for these guys is back in 2019, margins coming down, that’s competition. But we’re saying, hey, it’s going to go all the way up to 5%, and then we’ve got our balance sheet assumptions, tax rate assumption I’m sorry, then our balance sheet assumptions here as well. And so we’re coming back and saying, okay, so neutral scenario 18.57.623.

You saw the assumptions. Where does that play out? Well, that’s in the DCF model. And we go to the model here, and this model you’ll see, will go all the way out for 100 years.

It’s not because I’m making a prediction that far, right. It’s only because I am trying to make sure that we cast a large enough net to capture market expectations. Because sometimes, as you’ve seen, even with this one, in our default scenario, which is where we put in realistic expectations, it takes more than 100 years.

So in this situation, for square in the reverse DCF, we will change the default scenario here to neutral, which is the one we were looking at on the decision page. And you’ll see that these revenue growth rates change to what we showed on the forecast page. You’ll see that the margin changes to what we showed on the forecast page.

And effectively, what you get is a free cash flow model all the way through to where you get free cash flow every year. You get the present value of that. The cumulative present value accumulates over time.

The idea is that we run our model out into the future for as long as it takes. Here it was year 23 to get a price that’s closest to, but still less than the current stock price. So we kind of reverse engineer what the growth appreciation period has to be.

Pete, that was the point that I was trying to get across, because I know a lot of people will say, how’d you get the number that you’re going out to? That was a good explanation. And what’s so different about our model is that all the traditional models usually say, oh, we’re going to just look at five years, because I don’t want to predict farther than that. Remember, expectations investing is all about not predicting, but quantifying the implied prediction as reflected in the stock price.

That’s the quote of the day right there. That’s what everybody needs to understand, because a lot of people are chasing short term alpha right now. And that’s not reality.

That’s right. It’s all about quantifying the future cash flows implied by the stock price. Because you can calculate the value of a stock based on future cash flows.

So what we say is, okay, well, let’s start with that stock price. And Mobison and rappaport say this better than I do. Start with the stock price and work backwards.

What does the company have to do? What do you have to put into a model for that model to generate a value equal to the current stock price? And one of the key assumptions in this model, it’s really important if you’re ever building one of these that if people aren’t following this key analytical rule, it’s not really a reverse ECF, and that is that your terminal value cannot be a perpetual growth terminal value calculation. I’m getting a little geeky on you here. That’s okay.

Can you explain that in layman’s terms if you want? When people say, hey, I’m putting a model, I’m only building my model for five years, and I’m going to forecast cash flows. What they don’t tell you is that while that seems simple on the surface, they super overcomplicate it because they have some terminal value calculation that they use to capture all the growth after those five years. So they say they’re not forecasting cash flows, but they really are.

And when you adjust those terminal value calculations, because they’re simple ratios or growth assumptions, they effectively assume perpetual profit growth, which is not a good assumption. Right. So that kind of defeats what we talked about before with Amazon, with where is the growth appreciation period coming from in the business itself, which you just made a very big point before, multiple times the difference between the company and the stock.

That’s right. So our terminal value assumption or formula is a no growth assumption. It assumes that the year in which that calculation happens, that’s the last year for the company.

That’s why we build models that look at multiple forecast horizons or multiple growth appreciation periods. Each one of them come up with something else that would ignite a different or another growth appreciation period. Yeah, because I think we both agree that bringing in this dimension of time and duration of competitive advantage is enlightening.

It’s the real world. It’s literally the real world of competition. Right.

That’s exciting. I love that. It’s one thing to grow profits and do well for a short amount of time, but the law of competition means people are coming after you.

I’ve got one of my favorite concepts in our training class, and I got it from actually another guru in the space, bennett Stewart in the Eva book is the Investment Opportunity Schedule. And what it points out is that, look, if you got really high margins, you got high returns on capital. The number of companies that can achieve that are very few.

And by the way, the amount of time that is sustained is very low because competition is coming at you. And it’s a race to the bottom right on margins, unless you can do something that’s truly differentiated and value added. And you’re also not going to assume that that average cost of capital is going to remain the same either.

A lot of people got a real wake up call in the last couple of years, especially in the last 18 months when they went from zero to 15 months or 15 rates in a row, whatever that number was completely changed. The cost of capital. Yeah, that’s right.

The cost of capital was almost zero for a while. Which is why we saw this crazy speculative behavior. Yeah.

And the liquidity got pumped into the market. You had zero interest rates liquidity. It was the perfect storm.

It’s just kind of awful. At the end of the day, it’s why we have so much mal investment. We still really have to work our way through.

Yeah. A lot of people having no idea why that happened, complaining after the fact. When all that liquidity got sucked out, interest rates started to going up, and they were looking for people to blame.

Oh, yeah. Well, because they just want to believe that you can get rich for free and that you don’t have to be discerning, that companies can generate infinite returns on capital forever. Yeah.

That’s why I love these calls, because we’re trying to bring a little bit of common sense into what can be a pretty complicated process that you have to think through a little bit. You got to say what’s likely to happen, but in order to know what’s likely to happen, you have to have a framework to make that distinction in the first place. Yeah, I think that our stuff is super common sense, and that’s part of the reason I believe in doing this.

Pete and started new constructs to begin with, is that I knew that we could bring a very common sense, rigorous framework to the world, but we had to do all this back end, super complicated stuff to make sure the data was right and that people just didn’t want to do. But I believe in these concepts. Mobison had a huge impression on me.

I really believe in what they’re doing and talking about. I think it’s the right way to do things. Bring that in one more time.

And I think people benefit from this approach, but it’s extremely difficult to implement at scale. It’s extremely difficult to build one of these models for one company, but to do it at scale, it’s never been done before, but I think it’s super until now. All right, that was awesome.

I like ending with that quote. Maybe we’ll put that in, like, the highlight. All right, David, thank you so much for your time today.

We covered four stocks today that have upcoming earnings, and we started out a little bit at the beginning, looking at the overall picture of the market and talked about some of those market internals changing doesn’t mean the bull market is stopped. It means that you got to wake up and maybe make some decision here. So, David, thank you so much for your time again.

I really appreciate it. Any parting words today? Enjoyed it, Pete. Great talk.

And common sense. Excellent. All right, everybody, thank you so much.

We’ll speak to you soon. Anything that we talked about today.

Responses