The Daily Ticker Podcast: Meme Stocks Versus Value Plays 8-17-23

Everybody, welcome. Welcome to today’s episode of the Daily Ticker podcast. We are grateful that our friend David Trainer from New Constructs is here.

How’s it going, David? I’m doing great. Thanks for having me, Pete. All right.

Awesome. We got a big difference from the last month. We are now I don’t know if we’re necessarily going to say we are in a confirmed downtrend.

I know a lot of people are getting very uncomfortable with the quote unquote, stress free trading that we had the first six months of the year, and especially rocketing higher from May through July. And I know on our side, we were spending a lot of time saying, make sure you make what you’re supposed to. Right now, this is going pretty hard, pretty fast.

A lot of these stocks are getting way beyond what their normal moves are. And lo and behold, we’re in August and everybody’s getting chopped up. And here’s the big thing, and I don’t know if you see this on the investment side of things, but when you’re making what you’re supposed to, when it’s good, it’s a lot easier to be patient when it’s choppy.

And now we got a lot of people who are trying to make up for they didn’t take advantage of, weren’t prepared to make as much, was available during May through July, and now they’re pushing it a little bit and probably digging themselves an unnecessarily hole. And I know I could tell you this from longtime trading experience, that when you begin speculating trading, losses hit you like a punch in the stomach. However, once you start to have a little bit of a track record, what bothers you more is not making more in your winners, and the losses just become a business expense.

That’s a part of being a speculator, right? So it’s interesting to have members of the community who are kind of on both sides of the spectrum where they’re angry, they didn’t make what they were supposed to. Now they’re over trading, and it’s not a good spot to be in. But that’s the whole point of coaching, is to calm them down and say, there’s plenty of opportunity.

You don’t have to push it now. So I guess first is, do you think we’re in a reversal, or is this overvalued market just taking a break? Well, I thought we’ve been in a reversal a few times, Pete, but it turns out we reversed back. So 2022 was a nice sort of reversal.

In 2023, things have gone crazy. We’ve seen the meme stocks come back. I didn’t think we’d ever see that again.

Like, it’s the height of speculation and stupidity and riskiness, in my opinion. And I think that that’s just part of sort of calming the mean. It takes a while to choke out a know, there’s a lot dead, dead man spasms before someone finally gives up the ghost, you know what I mean? And I think that the Fed is not going to be out chopping heads off like maybe Volcker did.

They realize there needs to be a more slower, more deliberate approach to really change long term behavior. And that means you don’t just wipe people out, you make them feel pain slowly over a long period of time. Intermittent happiness and euphoria is going to kind of emerge.

And I think that’s where we are in the market now. And I think the downtrend we’re going to be experiencing over the next couple of months is the market finally digesting. The higher for longer is here to stay, and that’s going to change the paradigm around the economy and the stock market.

I know this is very opinion type thing, and obviously everything we talk about here is for educational purposes. I’ve been in the markets pretty much for 23, 24 years now, and there seemed to be a much slower pace to things kind of back then. I kind of feel like everybody, including investors, are chasing quarterly returns now as opposed to actually investing.

What are your thoughts on we all saw you read the book Flash Boys, right? I mean, high frequency trading or milliseconds, it’s a super short term market. I remember back in the early 2000s, my old boss, Michael Mobison pointed out a paper that his great colleague and a guy who Mobison introduced me to as well, al rappaport, wrote a paper in the wall street journal. Or an article in the Wall Street Journal pointing out that holding periods had gone from around seven years to less than a year on average.

That’s a huge difference, which was a big deal in the 90s or early two thousand s, I would say holding periods are in the days now. On average, if you take into account all the high frequency trading, they’re probably in less than a second on average because the high number of those trades that we see. So I think it’s a super short term oriented market.

So short term that people don’t believe that they need to take the time to understand fundamentals, which to your point, at the beginning of the meeting here, you were empathizing with how much it hurts people when they kind of start to lose on speculating. And I think that’s what I try to bring to people is some peace of mind that what you’re doing is based on solid ground. You’re not building castles in the sky.

That’s speculation. Solid ground is fundamentals. So if you see a setback, you want to probably buy more, as opposed to realize you waited too long to get out.

That kind of actually takes us to the next thing, which is overvalued versus it’s still going up. And I think that probably William O’Neill did the best job of this, where it’s not fundamentals or technicals. Even if you’re 100% fundamental, you still have to have some criteria that tells you this isn’t valid anymore.

There has to be everybody quotes. Well, Warren Buffett never sells a stock. Well, you’re not Warren Buffett, first of all.

If you get a margin call, you’re not Warren Buffett. So, again, everything here is for educational purposes. I don’t care if you’re just fully fundamental.

You still need a metric or a way of saying, my original thesis is no longer valid. And whether that’s technical, a change of earnings, a change of margins, whatever that happens to be, I think it’s just smart whatever time frame you’re trading. But specifically, we’re talking about investing in this particular moment.

And the reason I’m bringing it up is we had a lot of people come into our community, and we’ll go to Nvidia as an example. It was beautiful. It was absolutely amazing the way it was going up.

And those that were long and closing their eyes and just continuing to stay long kept getting rewarded. And now that it’s pulling back, those same people are wondering what they did wrong, looking for reasons why it’s happening, and they’re not factoring in the fact that the stock was up, what was it, 200% in six months? That’s not normal. It’s not normal.

And they can’t maintain that unless more AI mania comes out. But even still, speculation is about what’s likely to happen next and what’s the justifiable risk. And I think a lot of people put that second part out the window.

Agreed. Agreed. I mean, you’re talking about a fundamental framework, I think, Pete, where you understand value relative to cash flow, value relative to profits, the future profits implied by the stock price growth appreciation period that you and I have talked about.

And look, what is life without discipline? I think every mature human being recognizes that you have to have some discipline in your life. Without discipline, I mean, what, do we all walk around stabbing each other in the back? We all pee in our pants? Even at the most basic level, discipline is required to get through your life. And when you get into more sophisticated elements of life, discipline becomes even more mean.

You know, the highest levels of sports, the most sophisticated athletes right. Extremely disciplined about how they take care of their body. And I will tell you, successful investors are extremely disciplined.

Look at Warren Buffett, his discipline, and how it has defeated all the crazy whims of the last 25 years. I mean, people used to say during the tech bubble, I remember, oh, Warren Buffett’s a dinosaur. He doesn’t understand technology.

Well, you know what? People thought that for a year or so. And guess what? He was right. Oh, Warren Buffett’s.

Crazy. He doesn’t understand the housing market. Yep.

You know what he doesn’t understand? NFTs. He doesn’t understand crypto. He doesn’t understand blockchain.

He just keeps winning because his discipline helps him ignore a crazy Mr. Market or the fads of the. And what I like to help believe that we can help provide investors with is a fundamental backbone for discipline because we will show you exactly what the risk reward is when you compare profitability and valuation and understanding how much of a difference in the business the stock price implies in terms of future cash flows.

If the cash flows are here and the stock price says they’re going to go up to here through the roof as they did for Nvidia for a while, that’s a bad thing. An opposite could be a good thing, all that’s in context, but it gives you fundamental risk reward. And I think that should help people sleep well at night to know that, hey, when the music stops, which is what technical investing is, a lot of times it’s like just trying to figure out when the music stops and it’s difficult to do that.

But when the music stops, if you don’t have good fundamentals backing you up, you’re going to be feeling a lot of pain. Would you say, and again, I don’t want to put words in your mouth, but would you say fundamental risk reward is similar to what Ben Graham says is a moat where you’re getting that cushion when you actually buy at the right price? Very similar concept. Just we do all the math to make that actually much more than just a statement.

So what growth appreciation period is a measure of how wide the moat the market is giving the company credit for. So if the market is giving you a credit for 100 year moat, that’s maybe expensive, good luck with that. Or if the market’s giving you credit for zero moat, well then that’s good value, right? And then if you can conjuxtapose that to just how profitable the business has been, if it’s got a super high returns on capital, it appears it would be actually well positioned to have a strong mode because it’s making so much money.

It’s got good competitive position. Competitive, you do all the competitive analysis, that’s good risk reward, high returns on capital, strong competitive position taking market share, macro tailwinds and then a cheap valuation that’s getting buying companies that have a wide moat, but the market has not yet given them credit for that. When you just mentioned macro tailwinds, would that be sector specific macro tailwinds or just macro tailwinds in general? And what sectors would benefit from that? Both, right? I mean, if you can have like a larger macro tailwind or the overall economy and good down to the sector, down to the company, that’s your perfect alignment, right? You want to be able to check all those boxes.

That’s ideal. Takes patience and discipline to wait for those to come along because they don’t grow in trees every day. And by the way, what’s Wall Street trying to sell people on every day, Mr.

Market, every day. This is the next Amazon, this is the next Chipotle, this is the next Google. And they want you to believe that every day because guess what? They make money on your volume.

Right. Yeah. It’s funny you mentioned that 20 years ago to today, because something that a lot of people might not know to place a trade 20 years ago cost $200.

And until that wall came down, you actually couldn’t afford to make these kinds of in and out, in and out decisions because you actually had to factor the commission into the trade idea. Not anymore. Now you’re actually getting paid to trade.

Well, then, on top of that, there were the 100 share lot requirements. You couldn’t buy anything less than 100 shares at a time. Yeah.

Back then, OD lots were frowned upon by most broker dealers, actually. And now people are trading two shares of Nvidia. I’m like, what is that doing for you? Fractional shares.

Yeah, right. Even so. But your point is an excellent one, Pete.

It’s really important to keep in mind and ask yourself, why are they paying you to trade? Right. And really, that $200 trading cost was a benefit to most investors because it kept them from speculating, pretending they could be their own money manager. Yeah.

So with the market pulling back now, we’re seeing what to call the Magnificent Seven. All those guys are kind of getting beat up a little bit. Even Meta finally cracking down a little bit.

That stock is from 90 to almost 300 since this year started, so I’m calling it more profit taking than a reversal. Even today, the S and P 500 pulled back, closed near the lows broke below key moving average, 50 period moving average, but on lighter volume, three quarters normal volume. So they’re really not loading up into that position.

I believe the last time that we talked, we were talking about energy, financials and basic materials. Energy still at the top of my list right now. Pretty much every night I’m digging in that’s got the largest list of stocks with stacked order flow, basic materials cooled off a little bit for me personally.

Financials got hit a little bit this week on the they might downgrade. That’s another thing. They didn’t say they were downgrading, but they might downgrade.

Seems like the regional banks gapped down a little bit harder. But even Morgan pulled back, even with that amazing balance sheet. So I think this is a big part of understanding speculating, is where is the order flow moving in and out and following that around.

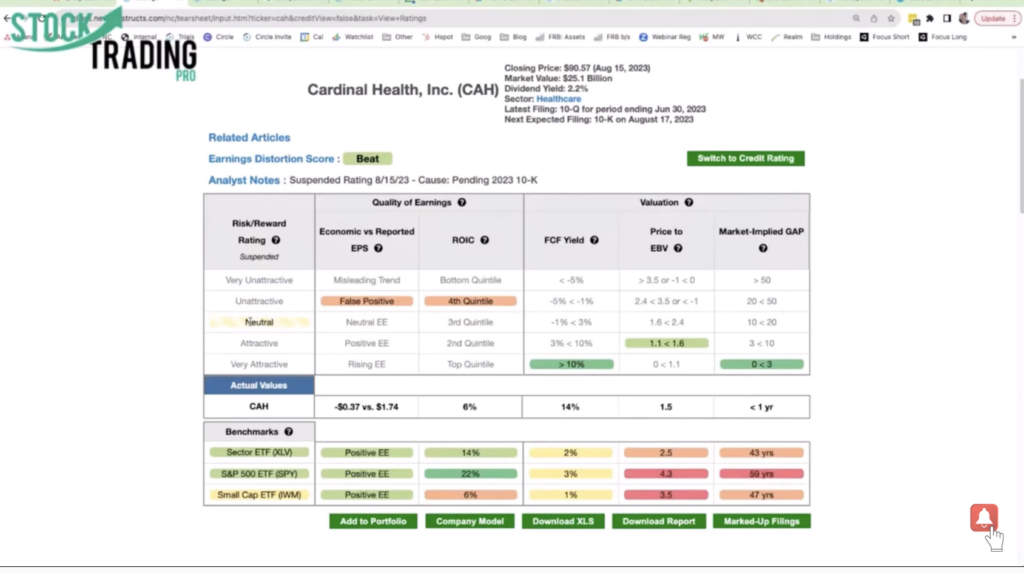

So we’re kind of seeing now a little bit of a migration over into healthcare right now. On my side of things, drug manufacturers, a little bit more specifically, aBVI and Amgen. But I know we just had earnings yesterday in one of the stocks that I’ve been watching for a while as well, cardinal Health.

Maybe you want to do a little bit of a run up on Cardinal Health. Yeah, we’ve been pretty bullish on healthcare for a while. In Spots.

In spots, right? And Cardinal Health is a really interesting one to do a deep dive on. So you’ll see that we’ve got a neutral rating. And I get this question all the time like, hey, David, I have a short strategy.

And it went from unattractive to very unattractive. Is that good? Or it’s there’s details. Oftentimes you can’t just take this rating, assume that it’s perfect gossip and just trade on that you need to kind of understand what’s going on.

And with Cardinal Health, I think a very interesting story is playing out because look, the valuation is good and attractive. 14% free cash flow yield. The price to economic book value is a little bit high, but the market applied growth appreciation period again, really cheap.

So, digging a little deeper into the rating breakdown and we see the economic earnings really steady. Yeah, a little bit of a downturn. Right.

But accounting earnings all over the case, all over the place. But we see a nice steady economic earnings number, which is helpful. Return on invested capital, similar deal.

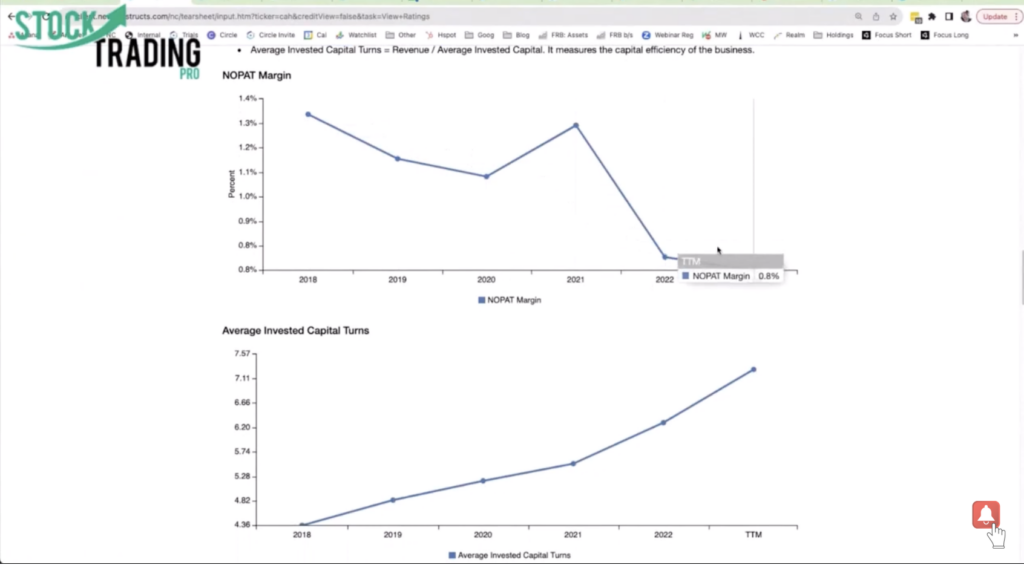

Right. And it’s headed up where people are going to get caught up and miss the boat. I think, Pete, is when you break down return on invested capital into its two prime drivers, and that’s the no Pat margin and invested capital turns.

So margins are going down, people. Boo hoo hoo, they hate that. Right.

But look, invested capital turns are going up, we’re seeing more balance sheet efficiency and that’s creating value enough to offset the decline in margins. So that you’re seeing an overall return on invested capital here in the trailing twelve months. That’s a really important picture.

So when you take that into account, you come back up here and you say, oh, you know what, maybe quality of earnings is on the upswing, it looks a little bit better. This neutral rating is closer to attractive. And we say this all the time.

The rating today is not what matters as much as where the rating is going to be in the future. Right. And so if we can anticipate a turnaround in the underlying economics and the stock looks cheap, that’s a great place to be.

So that’s my way of saying that Cardinal Health looks interesting. We have suspended the rating for a minute here because they’re late in getting us their ten K and it could be coming in any day now. But right now we think the stock could look a little bit more attractive and maybe that’s why it’s trading so well.

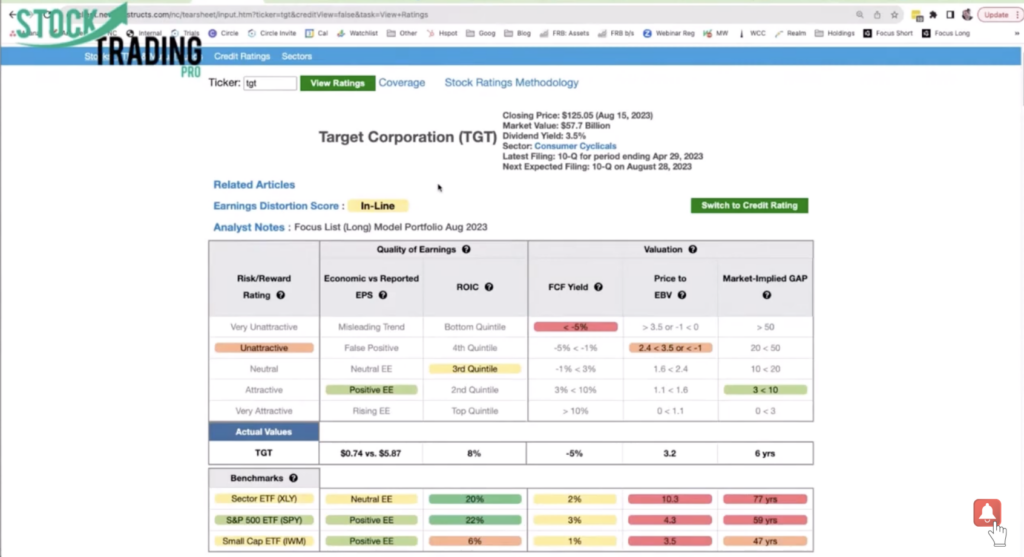

Okay, so you actually mentioned margins there before. Maybe we’ll hop into a different stock that has been beaten up a little bit. Target, over the last six months to a year kind of went sideways, broke down pretty big just before earnings came out.

Earnings and sales disappointed just a little bit, but the conversation shifted over to improving margin. So maybe we could take a look at that today through your lens. Yeah.

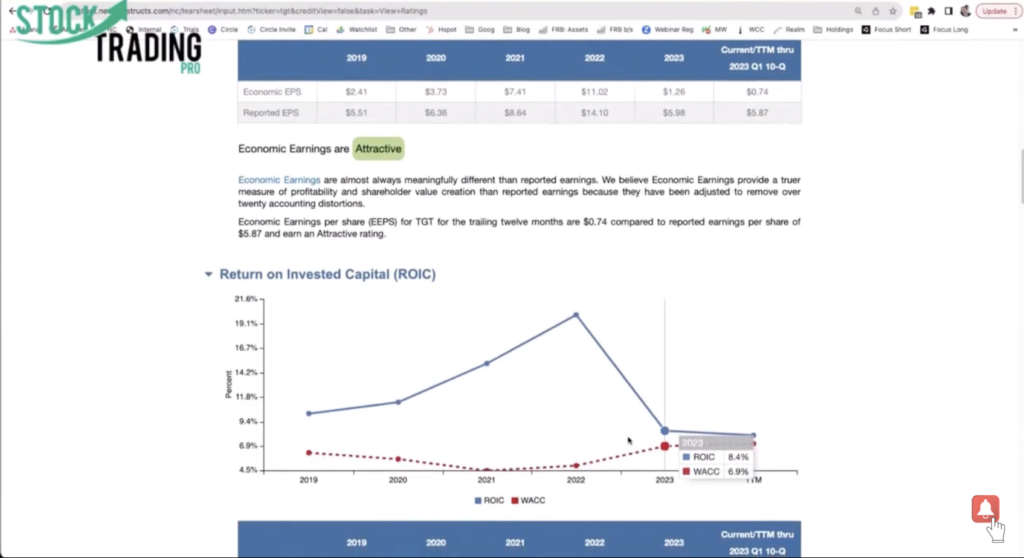

Target has been one of our focus list stocks for a while, and we just sort of saw it as like a premium version of where it’s where a lot of people would want to go otherwise. And they had a similar kind of business model, and they had a really high return on invested capital. And internally we’ve had to take a breath and say, okay, wait, are we sure still confident about our thesis? Because you can see with earnings here, economic earnings have come way down.

Return on invested capital took a nosedive after looking really good when we put it on the focus list, and things look great. This last year was a real punch in the gut. And so we’ve become not as bullish on Walmart because we think it’s fully valued.

And then we of course, turned our attention to Target to say, okay, target might be the same thing because it’s so competitive and growth is so hard to come by, you don’t want to assume that there’s a lot of easy upside in future fundamental improvements. And so we’re pretty bullish on the idea that margins are going to have flattened and maybe back on the rise. The earnings just came out today.

We’ll get the queue in the next day or so. We’ll update our model as soon as that happens. And if we can see margins kind of coming back, we’re going to remain more bullish than if we see margins continue to decline, because if targets effectively kind of lost its edge, we want to get out.

Okay, so that’s a good breakdown. So actually Walmart as well, coming up on Thursday, if I’m not mistaken, is scheduled to report tomorrow, and I believe it’s trading near all time highs, or maybe it just pulled back the last couple of days. With the rest of the market.

We saw probably around six months ago, there was a 160 price target put out on it, kind of danced around, got to that 160 price target, and it’s kind of been back and forth at that level for a while now, with I believe earnings are scheduled tomorrow morning, but I could take a look at that just to confirm that I don’t want to hold anybody holding that. I keep saying scheduled, definitely scheduled for tomorrow. I don’t remember if it’s before after hours, but it’s been dancing right around that 155, 160 level now for the better part of four months with earnings coming up.

Yeah, walmart is one where we just said, you know, it’s a little bit too expensive to justify the current stock price. They’ve got to bring their margins from 2.8%, which is the lowest since 1998, up to 3.9%.

Their ten year high grow revenue by more than 3% compounded annually. That’s above the last ten year CAGR of 2.6% for the next ten years.

So best ever margins better than historical growth for ten years to justify $156 a share. It’s important the company must outperform these expectations. If the stock is to offer upside to investors.

They got to do even better than that, like meaningfully better than that. They just barely beat it. Well then you’re going to go from 156 to 156.5,

you know what I mean? So it’s got to be a significant material beat. And so our take is that this is just a little bit too expensive. A lot of things are expensive and people just love to pile on and ride these expensive stocks up.

And whether it’s wayfair or other meme stocks, that feels good in the short term. But to your point, Pete, if it’s an investment in a castle built on sand or on speculation, people could be taking a lot of risk and potentially put themselves in a place where they’re going to be feeling a lot of pain and loss. Yeah, we saw that, I think probably the biggest stock that I’ve seen that in the last few years.

I don’t remember if you remember Kodak, when Kodak went from $6 to 68 in one day or two days at the most, it was one of those moves that was very reminiscent of the.com boom. And I show it to people all the time in our community about managing risk.

Yeah, it went from six dollars to sixty eight dollars in literally, I think, I’m pretty sure it was less than three days. And we had people asking, should I pile on? Should I pile on? This is not going to stop. And right back down to where it was and people that didn’t listen got caught holding the bag.

So my point is, and this is really like the biggest thing that I’ve really been kind of spreading the gospel on in my community. As much as we read the tape and read the order flow, the stocks that have the extra juice behind them, that juice which is sustainable and predictable, comes from the financials. And even if you’re not going to dive in to read balance sheets and income statements and cash flow and all that kind of stuff, there’s plenty of places, especially obviously new constructs, where you can get in there and get a little deeper dive and just have a little bit more conviction, because it doesn’t take a lot of profitable trades.

It takes the right trades that you really thought through. And technically a lot of people understand the technical side of the market. But understanding why you should be accepting that risk in the first place is really what separates somebody from holding the right idea.

And really your win loss percentage doesn’t mean anything because you hold one idea and you kick out all the small profits and small losses. It doesn’t take a lot of them, it takes the right ones. Yeah, that’s right.

Pete, for me, everything comes back to fundamentals. I mean, that’s where you start. That’s the basis, that’s your foundation.

If you’ve got that, you got an opportunity to build some discipline around a strategy without that, you’re driving at night without your headlights. So I just want to finish up on one thing because you’ve mentioned it now four times, because it’s something that very, very big on and you probably didn’t even realize you did it, is whether you’re talking about Warren Buffett or whoever it happens to be, there’s a structured way of looking at things. And you can only have discipline if you have that structured way, because if you don’t have a specific way of looking at the market or making an investment decision, then everything looks random.

And not only will you not know if that’s a good idea, but you’ll also have no idea if that changed. And I think that’s where a lot of people get caught, is, number one, they’re starving for this consistency in their market returns, and they don’t understand that the consistency they’re striving for actually comes from following their system flawlessly. But you can’t do that if you don’t have a system in the first place, which tells you it’s there or it’s not there, or it’s there and it’s changed.

And I think that’s really interesting. I couldn’t wait to finish up with that because you had mentioned it four times without saying those exact words. If you don’t have a structure or a systematic way of looking at whatever your investment is, then you’re just guessing at that point and hoping it moves in your favor.

And that’s obviously why we’re doing these podcasts. We don’t want anybody to feel that way and just kind of pointing, even if you just wake up and say, he’s right, I saw it on a scan last night, or I saw it on a podcast. No, you got to make your own decision.

You got to dive in a little bit deeper. It’s that structure that leads to the consistency. That’s something that a lot of people just don’t really know.

Yeah, I would call it a philosophy. What’s your philosophy? What is your overall philosophy about what investing means? Are you a gambler? Are you a speculator? Are you an investor? That’s one of the first things we teach our analysts. There’s a big difference.

An investor is someone who invests trying to earn a yield in the asset over its life. A speculator is somebody who’s trying to predict the day to day psychology of the market. And we would much rather be investors because we can measure cash flow, we can quantify the future cash flows baked into the stock price.

And with that, we can put together tangible, quantifiable, risk reward. And that’s something we feel like you can build a philosophy and a discipline around. And again, to your point, without it, the technicals potentially can be a mirage.

You need to understand why you want to take that technical risk or trust that technical strategy based on what the fundamentals have told you is good or bad or not. We had mentioned that off the air before that. Upst, while the recent rally it had was really nice, but it went from 32 to 72 right back to 32 in four days.

And stocks that have long term likely fundamentals, it’s not going to lose 50% of that value in four days. Yeah, Upstart gets a very unattractive rating on our system. No good fundamentals there.

Yeah, you’re right. Those are meme stocks. There are lots of meme stocks.

Wayfair is a meme stock. Tesla is a meme stock. I think Netflix is a meme stock.

And then there’s obviously the other ones that have come about since then. But these are stocks that trade unrelated to their fundamentals. That’s an important point.

I’m not even necessarily saying not to trade them, but there is a difference between trading and investing in them. And if you’re going to take it as an investment, then it’s a different way of allocating your capital than saying, I’m looking at the charts over this period of time. And if that chart changes, I’m going to change my bias.

Because what I was looking for leaning on changed. But if you’re going to call it an investment, that’s a very different story than it’s going up for the last three weeks. That’s right.

All right. Another good call. David, thank you so much for your time.

I appreciate it. My pleasure, Pete. Thanks for having me.

Have a great day, everybody.

Responses